Keep up-to-date with us and what's happening in the business world |

|

|

- 2025 Annual Accounts Questionnaires - Important Notices - How’s Your Work-Life Balance? - Xero Pricing Increase - 1 September 2025

- Xero Tip of the Month: Upload Multiple Bills at Once in Xero - Xero Assistance Programme (XAP) Ending 31 July 2025

- Welcome to the Team: Josh & Nik - Tax Question of the Month: Ring Fencing of Rental Losses – What Portion Can Be Claimed on the Sale of a Residential Property?

- IRD Upcoming Tax Payment Dates |

|

|

Accessing Questionnaires - For Clients Without a Xero Account:

We’ve received a few questions from clients who don’t currently use Xero about how to access our End of Financial Year (EOFY) questionnaire. To make the process as smooth as possible, we’d like to clarify how access works.

If you don’t have a Xero login, you’ll need to create one to access the questionnaire. This is not the same as signing up for a full Xero plan - it’s a free login, with no cost involved, designed specifically for accessing Ask queries and other features in the Xero portal. Setting up your login only takes a few minutes and helps keep your information secure.

To get started, simply click the button below. You’ll be guided through a few quick steps to set up your login and access the questionnaire. Alternatively, you're always welcome to use the previous system by downloading the questionnaire from our website (Services / 2025 Annual Accounts Questionnaires).

|

If you have any questions, concerns, or encounter any issues, please don’t hesitate to get in touch with our team on 04 970 1182 or email us at admin@aafl.nz — we’re here to help. |

|

|

KiwiSaver Changes:

Following the 2025 Government Budget announcement, several KiwiSaver changes have now come into effect - with more on the way in 2026 and 2028. If you employ staff, now is the time to review how these changes may impact your payroll, contributions, and employee entitlements.

Government Kiwisaver Contributions - Changes effective from 1 July 2025: - The maximum annual government contribution has been halved, from $521.43 to $260.72

-

Individuals aged 16 or 17 will now qualify for Government Contributions, as long as they meet other eligibility requirements.

- Individuals earning more than $180,000 of taxable income per year will no longer qualify for government contributions.

Upcoming changes to default employer and employee contribution rates: - From 1 April 2026 - Employer and employee contribution rates will increase from 3% to 3.5%.

-

From 1 April 2028 - Employer and employee contribution rates will further increase from 3.5% to 4%.

We’ll continue to keep you informed as more details become available. In the meantime, if you have any questions about how these changes may affect your business or need help preparing, please don’t hesitate to call us on 04 970 1182. We’re here to support you.

To learn more information about these changes, click the button below. |

Investment Boost - Tax Deduction for New Assets

In addition to the KiwiSaver changes, the 2025 Government Budget introduced a new tax incentive for businesses called the Investment Boost. This tax deduction is available to all Kiwi businesses, regardless of their size or industry.

Effective from 22 May 2025, businesses can now claim 20% of the cost of new assets as an immediate expense, with the remaining 80% depreciated as usual. To claim Investment Boost, the asset must be: - new or new to New Zealand

- available for the business to use on or after 22 May 2025, and

- depreciable for tax purposes.

You can also claim for: - new commercial and industrial buildings

- improvements to depreciable property (but not residential buildings)

- primary sector land improvements

-

assets arising from petroleum development expenditure and mineral mining development expenditure incurred on or after 22 May 2025 (except rights, permits or privileges)

- mixed-use assets.

There is no limit to the value of new investments you can claim Investment Boost for. You cannot claim Investment Boost for: -

second-hand assets that are sourced from New Zealand

- residential rental buildings

- most fixed-life intangible assets (such as patents).

You can claim the Investment Boost in your income tax return for the year in which the asset is purchased. To read more about the Investment Boost, click the button below. |

If you're planning to invest in new assets or equipment, the Investment Boost offers a timely opportunity. Talk to our team about how to make the most of this incentive - call us on 04 970 1182. |

|

|

HOW’S YOUR WORK-LIFE BALANCE? |

It’s great to be the boss - you can work any hours you like, right?

Unfortunately, for many business owners, that means long hours, plenty of stress, and very few breaks and holidays. Gallup reported that 39% of the owners they surveyed worked over 60 hours a week.

Owners often report they are unhappy with their work life balance, and after the challenges of the recent years you might find yourself thinking hard about your priorities. |

| |

|

Running a business and having a life

Can you run your business effectively and still have enough time left over to do the things you love? You’re the best judge of how much time your business needs, but don’t neglect your wellbeing. If you would like to take back some personal time, you could consider: -

Delegating – don’t try to do everything yourself.

- Saying no – not every project is worth taking on.

- Investing in systems – to reduce time on admin or paperwork.

-

Taking all your leave – find ways to have breaks and holidays.

- Maximising technology - making sure your systems are all integrated, and using AI where appropriate.

|

Working towards a balance

If you really can’t work less right now, try to build your business with a better balance in mind for the future. It’s important that you can step back at some point to take a holiday, travel, or spend time with family. Being tied to your business for more than 60 hours each week isn’t a sustainable way to take care of your health and higher profits aren’t worth that sacrifice. Also, any business that doesn’t allow the owner to step away is very hard to sell and worth far less than one that can run independently!

We'd love to help

Whether you want to improve your work-life balance now, or build your business to achieve it in future, we have ideas. We’ve worked with plenty of clients who need to reclaim their time, and we know it can be done.

Give us a call at 04 970 1182, drop us an email at admin@aafl.nz or come in for a chat - we’re here to help. |

XERO PRICING INCREASE - 1 SEPTEMBER 2025 |

|

|

We would like to inform you of upcoming changes to Xero’s subscription pricing, which will take effect from 1 September 2025. Xero has announced an increase to its pricing structure, and as a result, your September invoice may reflect a higher amount than usual.

New Xero Pricing (Effective 1 September 2025): - Xero Ignite plans remains the same at $35 per month

- Xero Grow plans increases by $8, bringing the new price to $83 + GST per month

- Xero Comprehensive plans increases by $11, bringing the new price to $110 + GST per month

However, as you know, we pass on our Xero Platinum Partner discount to all of our clients. With this discount, the new prices for your Xero subscriptions through All Accounted For, effective Monday, 1 September 2025, are as follows: -

Xero Ignite plans remains the same at $29 + GST per month

- Xero Grow plans increases from $56 to $59 + GST per month

- Xero Comprehensive plans increases from $73 to $78 + GST per month

For more information on the Xero pricing increase, click the button below. |

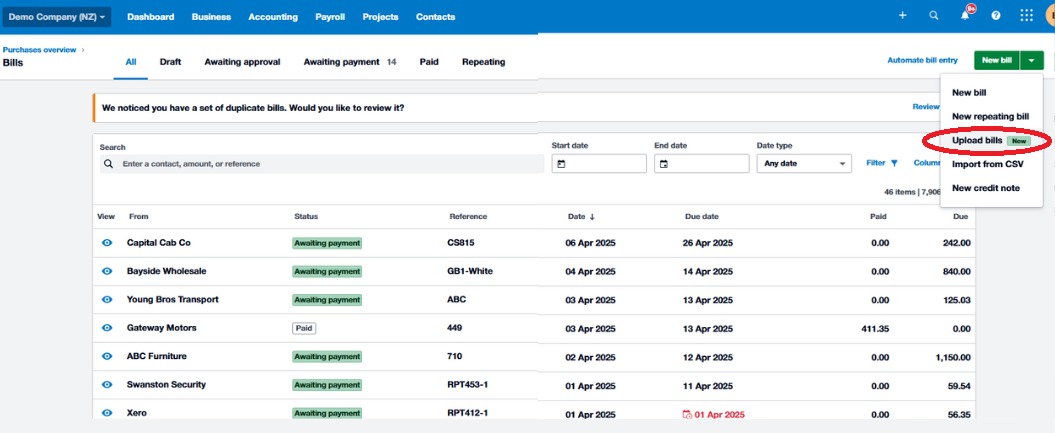

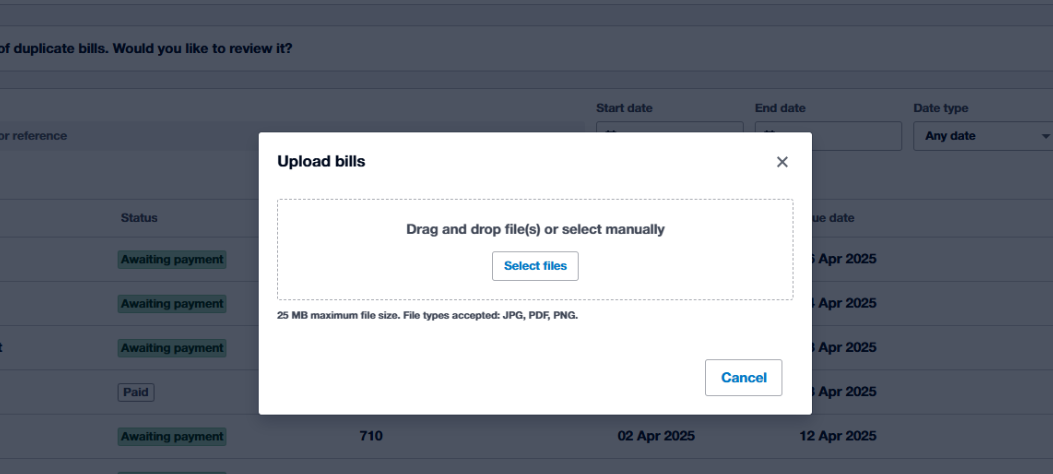

XERO TIP OF THE MONTH: UPLOAD MULTIPLE BILLS AT ONCE IN XERO |

Great news! You can now upload multiple bills at once in Xero.

Instead of uploading bills one by one, the Upload Bills feature lets you select and upload multiple files from your computer - or simply drag and drop them into Xero. This update makes managing large volumes of bills quicker and easier.

To upload multiple bills: 1. In Xero, go to the Bills section.

2. Click the dropdown arrow next to the "New Bill" button and select "Upload Bills." 3. Choose the files from your computer or drag and drop them into the upload window.

4. Click "Upload Files" |

|

|

XERO ASSISTANCE PROGRAMME (XAP) ENDING 31 JULY 2025 |

Xero has announced that the Xero Assistance Programmme (XAP) will conclude on 31 July 2025.

Please inform your employees, as some may have used the program in the past for mental health support or may have been planning to access it in the future. After XAP ends, customers will still be able to access professional wellbeing support at an exclusive discounted rate, thanks to Xero’s ongoing partnership with TELUS Health (formerly Benestar). |

|

|

We also recommend exploring other mental health resources, such as Small Steps.

Small Steps (smallsteps.org.nz) is a New Zealand based initiative that offers free digital tools and resources to help people improve their wellbeing - especially during times of anxiety, stress, or low mood. The tools are designed to be easily accessible and focus on promoting positive thinking and mindfulness. |

| |

|

To access Small Steps, click the button below. |

WELCOME TO THE TEAM: JOSH & NIK |

|

|

Josh is a local Wellingtonian with a strong foundation in accounting and a clear ambition of becoming a Chartered Accountant. After completing his undergraduate degree in 2020, including a minor in Accounting, Josh has continued to develop his expertise through the Chartered Accountants Foundation Programme. As our new BAS Accountant, Josh brings valuable hands-on experience from his previous role as Office Administrator at Rāroa Normal Intermediate School. In that role, he managed accounts receivable, prepared monthly financial reports, and supported the annual audit process. This role sparked his passion for accounting and confirmed his desire to build a long-term career in the profession. Outside of work, Josh enjoys spending time with friends and family, getting lost in a good fantasy novel, and cheering on the Hurricanes. Enthusiastic, organised, and eager to learn, Josh is already proving to be a great fit and we’re proud to support him as he grows in his career. |

|

Originally from Malaysia, Nik has called Wellington home for the past four and a half years. He holds a Bachelor of Commerce from Victoria University and joins our team as a BAS Accountant, bringing with him practical experience in supporting small to medium-sized businesses with financial reporting, tax compliance, and management reporting. Nik is passionate about transforming numbers into meaningful insights that help clients make confident, informed decisions. He is highly proficient in cloud-based platforms like Xero and is recognised for his collaborative style and talent for streamlining financial processes. Currently working toward his Chartered Accountant qualification, Nik is committed to continuous learning and professional growth.

Outside of work, Nik enjoys catching up with friends, exploring new eateries, and browsing his local shops. We’re thrilled to have Nik on board and look forward to the insight and energy he brings to the team. |

|

|

TAX QUESTION OF THE MONTH: |

QUESTION: During the 2024-25 income year a partnership sold a commercial yard and a residential rental dwelling. It had no other assets, and the partnership is to be wound up. The residential dwelling was never used as a main home by any of the partners.

The yard had rental income of $21,000 and expenses of $13,000 resulting in net rental income of $8,000 in the 2024-25 income year. The residential dwelling had rental income of $13,300 and expenses of $26,900 resulting in a net rental loss of $13,600. Overall, the partnership had a net rental loss of $5,600.

When the properties were sold, there was a capital gain on the yard of $21,000, and on the residential dwelling of $37,500. The sale of both properties was not caught by the land sale provisions in the Income Tax Act 2007.

What portion of the net loss from the residential dwelling ($13,600) can be offset against the partnership's other income?

ANSWER:

The deductions claimable on the residential dwelling for the 2024-25 year are limited to the residential rental income received of $13,300. The remaining deductions of $13,600 are ring-fenced and cannot be offset against the net rental income of $8,000 from the commercial yard. The deductions in relation to a residential rental property are subject to the residential ring-fencing rules in subpart EL of the Income Tax Act 2007. Under s EL 4(2), the amount of the deduction that can be allocated to an income year must be no more than the "residential income" for that income year.

"Residential income" is defined as the following types of income that a person derives for an income year in relation to residential land (s EL 3): - residential rental income

-

financial arrangements income from a loan denominated in a foreign currency

- depreciation recovery income

- taxable gain on sale of residential land (essentially, a gain from a residential land disposal that is subject to the land sale provisions), and

-

net income the person would have if their only income were income referred to in the above bullet points from other land held on revenue account.

In this case, the deductions claimable for the residential property are limited to the rental income of $13,300 derived from that property. The disposal of the residential property did not give rise to income under the land sale provisions and is not residential income.

The balance of the deductions of $13,600 cannot be offset against the net rental income or the gain on sale from the commercial yard as ring-fenced residential rental losses can only be offset against certain income from residential rental properties. The commercial yard does not qualify as a residential rental property. References

Income Tax Act 2007, ss EL 3, EL 4 |

|

|

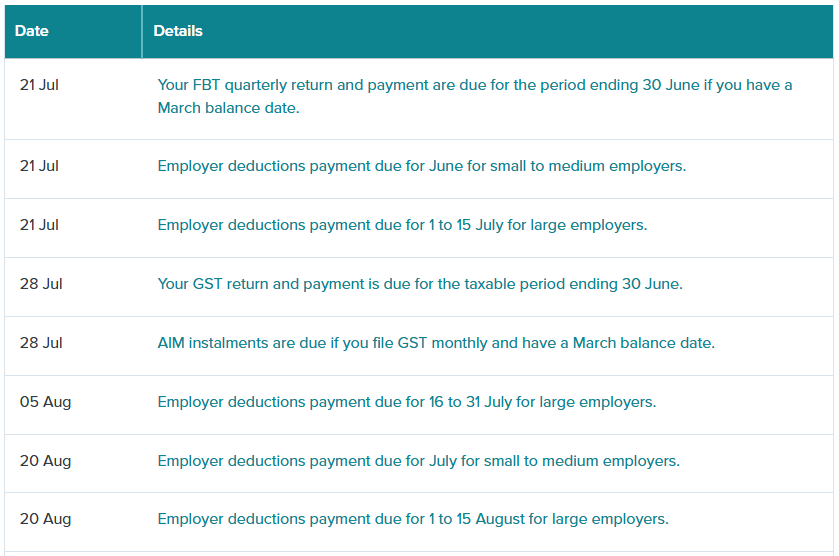

IRD UPCOMING TAX PAYMENT DATES |

|

|

|