October & November tax deadlines |

Remembering the filing and payment deadlines for your business can be challenging. And forgetting about tax payments coming up can seriously disrupt your cash flow planning. We have summarised tax deadlines coming up in October & November for you to prevent you from missing any deadlines and facing a penalty.

21 Oct - September Payroll taxes due for payment

- September quarter FBT Return due for filing and payment

- September RWT Return on interest or dividends due for filing and payment

28 Oct - Your GST return and payment is due for the taxable period ending 30 September.

-

Provisional tax payments are due if you have a March balance date and use the ratio option.

20 Nov - October Payroll taxes due for payment

-

October RWT Return on interest or dividends due for filing and payment

28 Nov -

Your GST return and payment is due for the taxable period ending 31 October.

- Provisional tax payments are due if you have a June balance date.

Make sure to plan for your tax obligations in your monthly cash flow forecasting. Reach out to your Walker Wayland Accountant if you need to review your forecast and look at options. For the full list of key dates click on the button below. |

|

|

GST on rental of holiday homes (such as Airbnb) |

From 1 April 2024, operators of electronic marketplaces like Airbnb and Uber are required to collect GST on behalf of suppliers, regardless of whether the supplier is registered for GST. Bookings made before 1 April 2024 are subject to the old rules. Do I need to register for GST?

If your income from your holiday home exceeds or is expected to exceed $60,00 in a 12-month period, you are required to register for GST. Requirements: You must notify your holiday home listing provider, such as Airbnb of your GST status. GST will be charged on the listing to your guests.

If GST registered: You will need to file GST returns with IRD. Income from your holiday home should be included in the ‘Zero-rated supplies’ box in the GST return, and you can claim GST on expenses as usual. As a result, you are likely to receive GST refunds. What If I am not registered for GST?

The booking platform will collect 15% GST on your income. However, they will pass on an 8.5% ‘flat-rate credit’ to you and pay the remaining 6.5% to the IRD. The 8.5% flat-rate credit represent the average amount of GST that IRD deem non-registered suppliers would have been able to recover as an input tax on goods and services purchased for their business. This ensures that non-registered suppliers are not disadvantaged by the new rules. For more information, please contact us or click on the button below: |

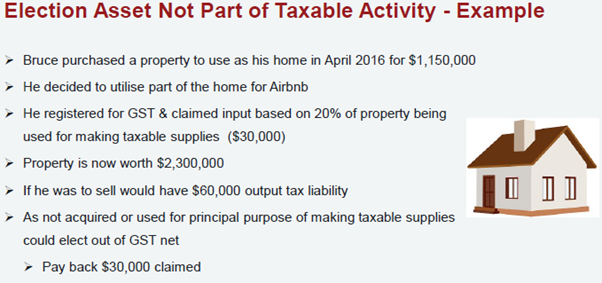

Time is running out—consider electing assets out of the GST net |

There is a restricted time limit to elect certain capital assets out of the GST net where those assets were not purchased for the main purpose of making taxable activity.

For any capital assets where a portion of GST has been claimed historically, the current default position upon sale is that a GST liability will be triggered for the Vendor, resulting in the Vendor having to pay 15% (if the zero-rating rules do not apply) on the full sale price. This is even if GST was only claimed in respect of part of the asset. This rule applies to all assets where GST has been claimed on at least part of the purchase price.

Transitional rule in section 91 of the Goods and Services Act 1985 has these conditions: A registered person previously claimed GST or acquired it as zero-rated supplies; and The property was acquired before 1 April 2023; and The property was not acquired for the principal purpose of making taxable supplies; and

The property was not used for the principal purpose of making taxable supplies. The election to apply this rule must be made to the IRD before 1 April 2025. From 1 April 2025, this opportunity to elect assets out of the net will be gone and any subsequent sale will be treated as subject to GST.

If this sounds like you, please contact us as soon as possible. The deadline for making this election is fast approaching. |

FIF Rules and Taxation of Foreign Share |

If you own overseas shares, you may need to report FIF income based on your foreign portfolio movements. You may be required to report this income to IRD if your total cost of the shares in foreign companies in NZD is greater than $50,000. Keep in mind that “foreign companies” excludes certain Australian resident firms listed on the ASX.

If you are required to report this income, there are two common methods used by investors to calculate this: Fair Dividend Rate (FDR) and the Comparative Value (CV) method.

The FDR method is calculated as the opening value of your portfolio at the beginning of the income year multiplied by 105% with adjustments if shares are purchased or sold during the year, the rationale for this is that the 5% uplift is meant to capture the dividends you may have received. The CV method compares the opening and closing value plus adjustments for share sales or purchases and distributions received. The performance of your portfolio should be considered when deciding which method to use. For instance, if your portfolio is in a loss position during the income year, the CV method may be favourable. The choice of method doesn’t apply to all entities, so it will depend on your personal situation as to which method is available to you.

Please note if you are reporting FIF income, the foreign dividends you have received will be excluded from your tax return, as they are considered to be captured by the FIF income. The above is a general brief overview of the rules on taxing foreign shares, please speak to your Walker Wayland accountant for more information. |

New Xero plans - effective 12 Sep 2024

Xero is moving subscribers to the new plans in phases, taking into account the subscriber’s current plan (and any add-ons) and recent feature usage (that is, Xero Expenses and/or Xero Payroll).

A summary of the plan migrations & increases *prices are GST inclusive • Starter $37.95 p/m > Ignite $40.25 p/m ($2.30 increase)

• Standard $81.65 p/m > Grow $86.25 p/m ($4.60 increase) • Premium $108.10 p/m > Comprehensive $113.85 p/m ($5.75 increase)

• Ultimate (old) $120.75 p/m > Ultimate (enhanced) $129.95 p/m ($9.20 increase)

Xero has also simplified the partner plans from three down to two (Ledger and Non-GST Cashbook will remain unchanged). These partner plans are only available for purchase by accountants and bookkeepers.

Ledger $4.03 p/m > Ledger $4.03 p/m (no increase) Non-GST Cashbook $18.40 p/m > Cashbook $18.40 p/m (no increase)

GST Cashbook $28.75 p/m > no longer available, clients currently on this plan will most likely move to the Ignite $40.25 p/m ($11.50 increase)

For more information, click on the button below. |

Making payroll admin easier with flexible working patterns

Payroll processing in New Zealand just got easier in Xero. You can now specify a work pattern of up to two weeks in length for employees, which gives you more flexibility in defining their working hours. This allows for more precise tracking and more accurate leave accruals. Additionally, annual leave is now displayed in weeks, eliminating the need for adjustments when work arrangements change. These enhancements will streamline processes, reduce manual tasks, and ensure greater legislative compliance.

Input the bank statement ending balance in the Bank Rec Summary Report for easier monthly review

In the Bank Reconciliation Summary Report, New Zealand customers can now input bank statement ending balances, to help identify any discrepancies and ensure the bank balance matches the calculated statement balance in Xero before publishing the reconciliation for the month. This will make monthly accounts reviews easier, saving you time and effort. |

|

|

Whilst most business owners are familiar with the need to produce financial statements and tax returns that reflect the historic position and performance, so as to meet compliance standards and ensure tax obligations are satisfied, it can also be very helpful to look towards to the future.

Here at Walker Wayland, we use a powerful 3-way business modelling software called Castaway, which enables us to produce financial forecasts and budgets with a forward focus. Using Castaway, we can produce integrated forecast profit and loss statements, balance sheets and cashflow statements, for periods up to 5 years. |

|

|

There are many reasons why a business owner may wish to produce integrated forecast statements.

1. While profit and loss statements measure historic financial performance, they do not always reflect the cashflow movements in real life. It is not uncommon for a business profit and loss statement to show profits, while the cashflow is running at a deficit. Integrated statements can help business owners to identify where the cash has actually gone, and where it will be coming from (and going to) in the future, thereby helping them to plan cashflows, and to budget accordingly (especially if there are big projects on the horizon).

2. Business modelling can also help business owners to better understand their own business, and to identity both potential growth opportunities, and threats to the business. Using software such as Castaway can enable business owners to predict future performance based on different variables, so that they can focus their strategies and take advantage of opportunities - or respond appropriately to challenges - as they arise. 3. Alternatively, if a business is seeking to obtain finance from banks or other lenders, forecasts can help to predict future cashflows and profitability, and thereby support lending criteria. Likewise, forecasts can be very useful if a business is looking to expand or raise finance through selling shares or additional capital to outside investors.

4. Castaway integrates with most commonly used accounting software, such as Xero and MYOB, so that we can incorporate your actual historic results, into your projections. Please get in touch with us to discuss how using Castaway Forecasts can benefit your business. |

This month we would like to introduce Blacklock Rose, a fellow Auckland / Northland based member of the Walker Wayland Australasia Network, a boutique firm specialising in insolvency matters. Blacklock Rose was formed 16 years ago by Garry Whimp to provide insolvency solutions to businesses in distress. Ben Francis joined the team in July 2023 and brings a wealth of knowledge from his years in the industry, both in New Zealand and Australia. Blacklock Rose are an expanding practise located in Northland and now with an office in Auckland. Their team has an abundance of knowledge in insolvency matters including liquidation, voluntary administration and receivership.

These are busy times, and we find ourselves in a growth industry. Garry and Ben are frequently being asked by accountants and lawyers to meet with clients to advise on the best ways forward for their company and the stakeholders involved. Blacklock Rose currently have insolvency appointments which range from a small cafe to a publicly listed company. The job can be complex but is never dull and it seems that no two appointments are the same. For advice regarding insolvency, please contact Garry Whimp. |

Garry Whimp

Founder & Managing Director |

P O Box 2175 Auckland 1140 |

|

|

|