Keep up-to-date with us and what's happening in the business world |

|

|

|

- 2026 Budget Announcement

- Cutting costs or increasing your prices? We can help - Xero Tip of the Month: The Refreshed Xero Accounting App Navigation

- Welcome to the Team: Lavina - Tax Question of the Month: Case Study - The Incorrect Tax Code - IRD Upcoming Tax Payment Dates

|

|

|

|

Budget 2026 economic outlook was framed as cautiously steady, with the Government signalling a focus on maintaining fiscal discipline while supporting gradual improvement in economic conditions. While cost-of-living pressures and broader global uncertainty remain present, the overall message pointed to a gradual and uneven recovery and improving conditions over time.

Capital and operational investment remained a key feature of the Budget, with continued focus on core priorities including infrastructure, health, education, and essential public services. Alongside this was an ongoing emphasis on lifting productivity, supporting economic growth, and strengthening long-term resilience to help deliver more sustainable outcomes in the years ahead. The big key takeaway from Budget 2026 is the Government’s forecast that New Zealand will return to surplus in 2028/29, with debt expected to begin falling as a share of the economy over time, reflecting a longer-term focus on restoring fiscal stability and strengthening the country’s financial position.

Below, we have summarised the key announcements and what they may mean for you.

Budget Overall - Government forecasting a return to operating surplus by 2028/29.

- Continued focus on fiscal discipline, spending restraint, and reducing government borrowing over time.

-

Ongoing investment in infrastructure, health, education, and public services.

- Continued emphasis on improving productivity and supporting private-sector-led economic growth.

Further simplification of selected tax compliance requirements, particularly around the simplification of FBT rules for motor vehicles and the increase in the Foreign Investment Fund (FIF) de minimis threshold from $50,000 to $100,000.

Debt expected to decline gradually as a proportion of GDP over the forecast period.

Below is a summary of the key budget announcements in more detail: Business Initiatives

On the whole, there were very few major announcements for the Kiwi businesses. Continued investment in infrastructure projects will mean more opportunities for the construction and engineering sectors, but measures to help support Kiwi small businesses through their current economic challenges were thin on the ground. Announcements that may impact business owners include: Taxation: - Changes to Fringe Benefits Tax (FBT) for motor vehicles: Budget 2026 simplifies fringe benefit tax (FBT) rules for private motor vehicle use by removing the requirement for detailed logbooks and replacing it with a ‘close enough is good enough’ approach for logging vehicle usage

-

Investment Boost continues to be available for New Zealand Businesses.

-

Budget 2026 introduced changes to Foreign Investment Fund (FIF) rules to help retain talent by extending the new FIF “revenue account method” method on unlisted shares to all New Zealand taxpayers, ensuring tax is paid only on realised gains and actual dividends, and by increasing the de minimis FIF threshold for overseas investments from $50,000-$100,000.

|

Charities and Non-Profit Organisations:

Changes to the tax rules for charities and non-profits: The Government is improving tax rules for the charitable and not-for-profit sector to ensure fairness and resilience. Key changes include: - Increasing the amount of net income a not-for-profit organisation can earn without paying tax from $1,000 to $10,000.

-

Ensuring the donation tax credit scheme remains financially sustainable by capping eligible donations at $100,000 per year. This will also limit tax planning risks that can arise when a donor makes a gift to a charity they control themselves.

-

Allowing donors to receive their donation tax credit refunds throughout the year in certain circumstances, rather than waiting until the end of the tax year.

- Allowing donors to gift their donation tax credit to a charity.

Ensuring that membership subscriptions and levies received by not-for-profits remain non-taxable Infrastructure Boost Significant ongoing investment in transport, water, schools, hospitals, and other public infrastructure projects.

Continued support for major capital projects aimed at addressing infrastructure deficits and supporting long-term economic growth. Increased infrastructure activity expected to support employment and create opportunities across a range of industries. Focus on delivering projects more efficiently and attracting greater private sector participation in infrastructure development.

Education Initiatives Additional funding to support classroom learning, school operations, and educational outcomes. Continued investment in school property upgrades and maintenance programmes. Support for vocational education and workforce development initiatives to help address skill shortages. The government is ending final-year Fees Free tertiary education while doubling the number of Trades Academy places for school students.

Ongoing focus on improving educational achievement and preparing New Zealanders for future workforce needs.

Health

Increased funding for frontline health services and workforce capacity. Continued investment in hospitals, health infrastructure, and service delivery improvements.

Focus on reducing waiting times and improving access to healthcare services. Ongoing support for mental health and community health initiatives.

Impacts for Individuals No broad-based personal income tax cuts were announced.

Continued focus on managing inflationary pressures and supporting economic stability.

Changes to investment taxation rules may benefit individuals with overseas investments.The de minimis threshold for the Foreign Investment Fund (FIF) rules is increasing to $100,000, potentially removing compliance obligations for those with modest overseas shareholdings.

Improvements to donation tax credit administration may provide greater flexibility for charitable giving allowing donors to receive refunds during the year and the ability to gift their tax credit directly to a charity.

The Government's longer-term fiscal strategy is aimed at creating a more stable economic environment for households and businesses alike.

If you wish to discuss how any of the budget announcements might impact your business or yourself, please contact any of the team at All Accounted For, admin@aafl.nz or 04-970-1182. |

|

|

|

CUTTING COSTS OR INCREASING YOUR PRICES? WE CAN HELP |

With many businesses expecting a lower profit this financial year, the more prepared you can be for the unexpected, the better.

Managing expenses is a good idea at any stage in your business, and reviewing your pricing can also help improve your margins and support long-term sustainability. The challenge is knowing where to start. |

|

| |

|

Before making significant changes, it pays to take a closer look at how your business is operating, where money is being spent, and whether your pricing still reflects the value you provide. Small adjustments can often make a meaningful difference to your bottom line.

Smart ways to get your costs under control

Cashflow has been a big issue for thousands of businesses this year, and when the money's not rolling in, it can help to rethink your costs. To do it effectively involves more than just keeping an eye on outgoings. It's about looking at all the moving parts of your business to see if your systems (or lack of them) are costing you unnecessarily. Here's how: -

Muck in - Do a cost control audit to work out where your biggest cost centres are and review the systems you have in place to manage them.

-

Be aware - Don't just slash expenses without considering the impact. Track costs carefully and look for opportunities to streamline spending or achieve the same result in a more cost-effective way.

-

Unite your team - Bring everyone together to monitor and analyse inputs and expenses. If you're reviewing or developing systems, seek feedback from the people using them every day.

-

Look to your peers - How do your costs compare to others? If a business of a similar size is performing well while spending less, explore what they're doing differently.

-

Seek advice - Whether you've identified some problem areas or you're unsure where to begin, talking with your advisors (that's us!) can help you determine the best next steps.

How can I put my prices up without losing customers? If you need to change your pricing to make ends meet, be honest and up-front with your customers at all communication points. -

Make it clear on your website and social media that prices have changed and explain why.

- Send an email to let your customers and suppliers know about any changes in advance.

-

If you're meeting customers face-to-face, ensure they're aware of any price increases before they're invoiced. No one likes an unexpected surprise.

- Support your team with clear information so they can confidently explain any changes and continue delivering a great customer experience.

-

If you're concerned about customer reaction, consider introducing increases gradually across products or services over time.

Get in touch if you'd like us to help analyse your margins, review your expenses, and identify opportunities to strengthen your business performance. |

|

|

|

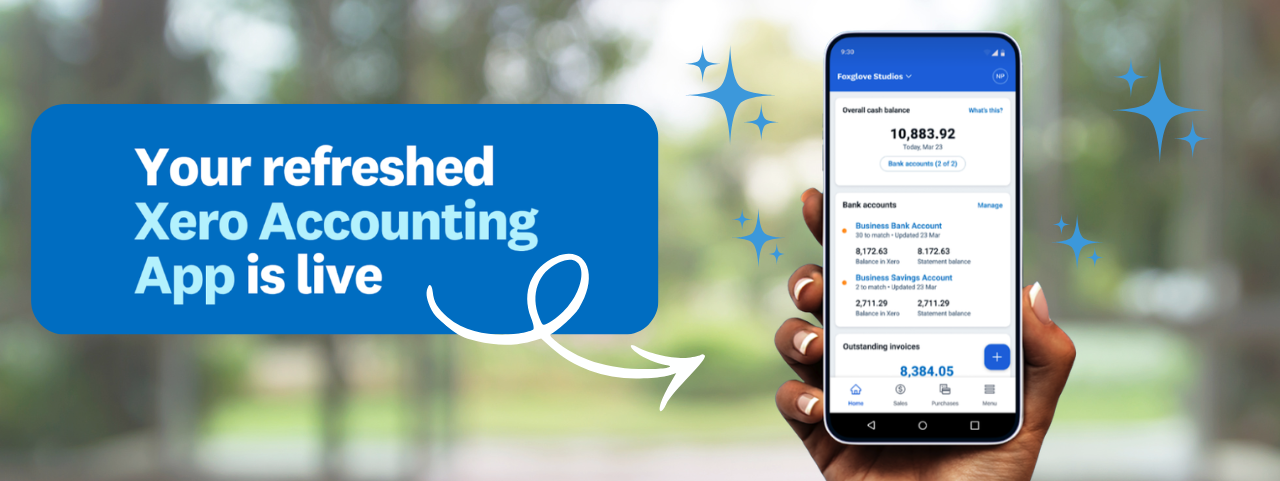

XERO TIP OF THE MONTH: THE REFRESHED XERO ACCOUNTING APP NAVIGATION |

Keeping on top of your finances while you’re out and about just got easier! Xero has refreshed the Accounting App experience to make it simpler for you to access key features and complete everyday tasks from your mobile device.

The updated layout improves how you move between core areas, helping you find what you need faster and stay on top of activity wherever you are.

What’s Changed - The key improvements include: - A simplified bottom navigation to help you move between key areas more easily

- Home as the main dashboard view for a clearer overview experience

-

Key functions such as invoices, bills, bank accounts, and contacts accessed through a streamlined Menu for easier navigation

This makes it easier for you to quickly locate what you need, whether you’re processing invoices, reviewing transactions, or checking account activity. How to Use the Refreshed App Navigation: -

Open the Xero Accounting App on your mobile device

- Use the simplified bottom navigation to move between key areas

- Tap Home to view your account overview

-

Access core functions such as invoices, bills, bank accounts, and contacts via the Menu

- Navigate directly through the Menu rather than switching between multiple screens or tabs

Next time you’re using the Xero mobile app, take a moment to explore the updated layout, it’s designed to help you move through tasks more efficiently, wherever you’re working from. |

|

|

WELCOME TO THE TEAM: LAVINA |

|

|

|

| Meet Lavina, our new Client Services & Administration Coordinator! Lavina brings over five years of experience in client services and logistics, with a strong focus on coordination, communication, and supporting day-to-day operations. After moving to New Zealand in December 2022, she gained valuable insight into the local finance and tax environment through her time at Inland Revenue. |

|

|

|

Originally from India, Lavina holds a Bachelor’s degree in Electronics and Communication Engineering. Her diverse background has helped her build a practical, solutions-focused approach to her work, along with a strong ability to adapt to new systems and environments.

She is excited to be joining the AAF team and looks forward to continuing to grow her skills while supporting clients and the wider team. Outside of work, Lavina enjoys painting, cooking, writing poetry, and shopping. |

TAX QUESTION OF THE MONTH: |

SCENARIO: Robert is a salaried employee earning $70,000 per year from his full-time job. For the entire 2025/26 income year (1 April 2025 to 31 March 2026), he correctly used the 'M' tax code for this job.

On 1 October 2025, six months into the income year, Robert took on a second, part-time job earning an additional $20,000 for the remainder of the year. When filling out his tax forms for the new job, he mistakenly selected the 'M' tax code again, instead of a secondary tax code.

It is now June 2026, and Robert has just received his income tax assessment from Inland Revenue. He is surprised to find he has a significant tax bill to pay. QUESTION: Why does Robert have tax to pay, and how much is it? What should he have done differently? |

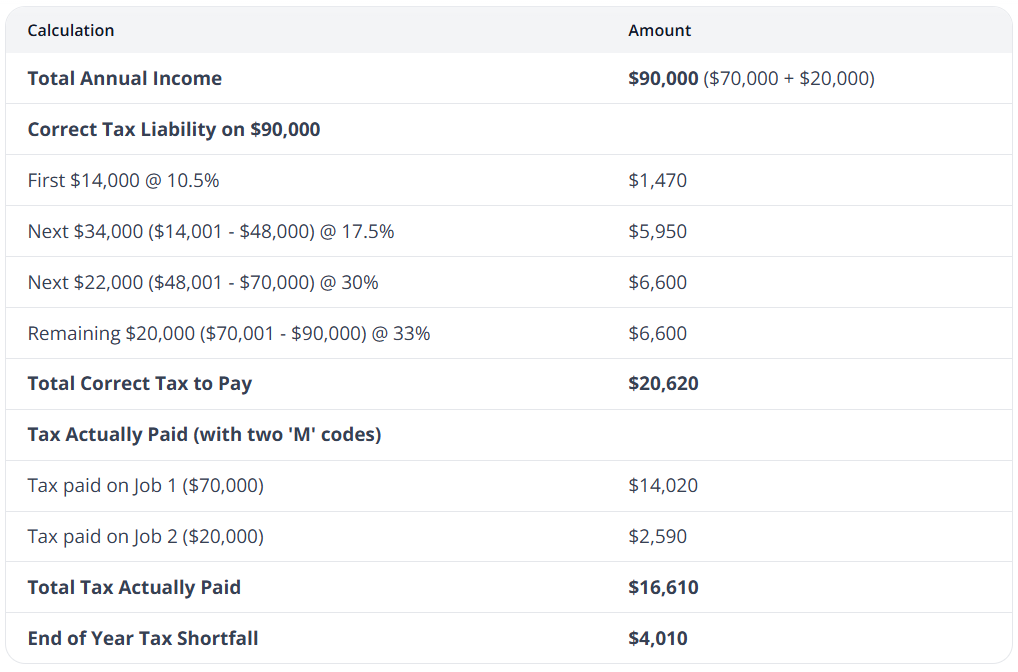

ANSWER: Analysis and Solution

This issue arises from using the primary tax rate for two separate jobs concurrently. Each employer's payroll system, when applying an 'M' code, calculates PAYE on the assumption that it is the employee's only source of income, thereby applying the lower tax brackets to that income.

The Problem with Using Two 'M' Codes

When an individual has two jobs and uses an 'M' code for both, they are effectively claiming the tax-free threshold and lower tax brackets twice. This results in less tax being deducted from their total income than is legally required, creating a shortfall by the end of the year. This is a common situation for taxpayers with multiple sources of income. Calculation of Robert's Tax Position Here is a breakdown of the tax that was paid versus the tax that should have been paid for the 2025/26 income year. |

Robert's tax assessment from Inland Revenue will show that he has $4,010 of tax to pay by the terminal tax date (usually 7 February of the following year). What Should Have Been Done?

To ensure the correct amount of tax was deducted, Robert should have used a secondary tax code for his second job. Based on his total income of $90,000, his main job would use the 'M' code, and his secondary job would use the 'SH' tax code (for total income between $70,001 and $180,000). The 'SH' code would have instructed his second employer to deduct tax at a flat rate of 33%, which is Robert's correct marginal tax rate. This would have prevented the year-end shortfall.

Alternatively, if his income was less predictable, he could have applied for a tailored tax code from Inland Revenue. A tailored tax code sets a specific withholding rate to ensure the correct amount of tax is paid over the year, aiming for a nil balance at year-end.

Conclusion and Client Advice - Acknowledge the Shortfall: Robert has a legally payable tax debt of $4,010 due to using an incorrect tax code.

-

Correct the Code Immediately: He must provide his second employer with a new tax code declaration form (IR330) showing the correct 'SH' code for all future payments.

-

Plan for Payment: He needs to arrange payment of the outstanding tax by the due date to avoid penalties and interest.

-

Future Vigilance: This scenario highlights the importance for clients with more than one source of income to select the correct tax codes to avoid unexpected tax bills.

For more information on individual tax obligations and codes, you can refer to Inland Revenue's guidance. The rules for calculating and paying tax are primarily contained within Parts B and R of the Income Tax Act 2007. |

|

|

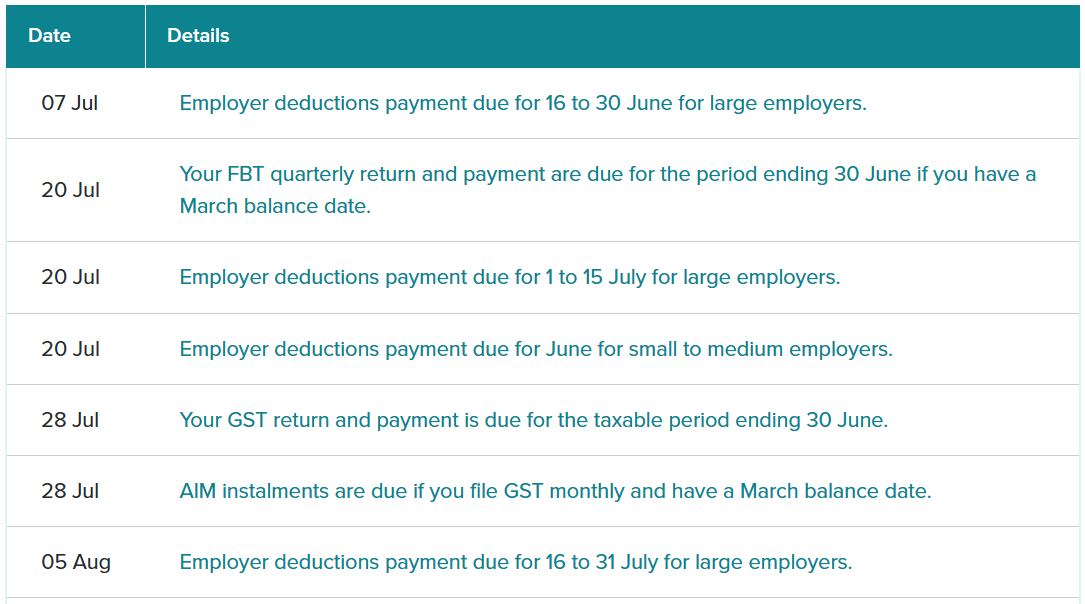

IRD UPCOMING TAX PAYMENT DATES |

|

|

|

|