Investment Boost Scheme - Fishhooks |

Announced on 22 May 2025 as part of Budget 2025, the Government has introduced a new “Investment Boost” scheme aimed at encouraging business investment. This initiative allows a 20% tax deduction on the cost of qualifying new investment assets acquired from 22 May 2025 onwards. Key highlights - The deduction applies to income for the financial year, reducing tax payable.

-

It does not result in an immediate refund or credit at the time of purchase.

- Several important conditions and exclusions apply.

What qualifies as a new investment asset? - Depreciable property and improvements to depreciable property

- Improvements deductible under farming, horticulture, aquaculture and forestry rules

- Assets acquired with petroleum or mining development expenditure

Excluded assets under s DI 4(b) of the Income Tax Act 2007 include: - Dwellings (including residential properties)

- Fixed-life intangible property

-

Petroleum privileges/permits

- Mining rights/permits

Assets that do not decline in value (e.g., branding, patents, customer databases, land) are also excluded. Tip: Ensure correct classification before claiming the deduction.

Availability for use The deduction is only available for assets that become “available for use” on or after 22 May 2025. -

An asset is considered available when it can be used to derive income.

- Assets under construction or awaiting compliance (e.g., websites, buildings) are not eligible until ready for use.

Depreciation recovery income If an asset is sold for more than its adjusted tax value, the excess is treated as depreciation recovery income and is taxable. -

Adjusted tax value = original cost minus depreciation and investment boost deductions

- Sale proceeds exceeding this value trigger taxable income

Used assets & prior use - Assets previously used in New Zealand are not eligible.

- No deduction for second-hand vehicles or equipment used domestically.

- Imported assets not previously used in NZ may qualify.

Mixed-use assets Residential dwellings are excluded, even if used for commercial purposes.

Mixed-use properties (e.g., shop with residential upstairs) may qualify for a partial deduction based on percentage of commercial use where the property has not been used previously.

Fixed-life intangible property Although amortisation is available for certain intangible assets, no investment boost deduction applies to: -

Fixed-life intangible assets (e.g., software licenses, IP rights)

- These are explicitly excluded under s DI 4(b)

|

August & September 2025 Tax Deadlines |

Remembering the filing and payment deadlines for your business can be challenging. And forgetting about upcoming tax payments can seriously disrupt your cash flow planning. We have summarised tax deadlines coming up in August and September for you to prevent you from missing any deadlines and facing a penalty. 5 Aug

20 Aug 28 Aug 5 Sep 22 Sep 29 Sep 30 Sep

Make sure to plan for your tax obligations in your monthly cash flow forecasting. Reach out to your Walker Wayland Accountant if you need to review your forecast and look at options.

For the full list of key dates click on the button below. |

Tax residency update - IRD releases new guidance |

The IRD has recently released updated guidance (IS 25/16: Tax Residence) on how tax residency is determined for individuals, companies, and trusts. The aim is to provide a clearer and more structured interpretation of the rules, drawing on recent case law and practical scenarios. Please note: These are general guidelines only. Tax residency is a complex area and depends on your personal circumstances. If you’re unsure about your status, feel free to get in touch with us for tailored advice.

Individuals: focus on habitual residence An individual is a tax resident in New Zealand if they meet either of the following two tests: -

The permanent place of abode (PPA) test

- The 183-day rule (being present in New Zealand for more than 183-days in a rolling 12-month period)

While the legislation around the 183-day rule and permanent place of abode (PPA) remains unchanged, the new guidance puts more weight on habitual residence factors when applying the PPA test.

Key points: - A “permanent place of abode” is where a person habitually resides, even if they spend time overseas.

-

Ownership of the property is not essential — it could be rented or owned by a family member.

- The test focuses on enduring ties, not temporary stays.

- IRD will assess:

-

Intentions

- Family and social ties

- Use of the property

- Other factors connecting you to New Zealand

Transitional residents: watch out for these triggers The transitional residence rules are still in place, but the updated guidance highlights some new risk areas: -

Claiming certain government benefits (e.g. Working for Families, Best Start) can end your transitional residency early.

- FamilyBoost payments are not considered government benefits.

-

A “familiarisation trip” to New Zealand before relocating permanently could backdate your residency to your first arrival.

Companies: control still matters

The four residency tests for companies remain the same: - Incorporated in New Zealand

- Head office in New Zealand

- Centre of management in New Zealand

-

Control by directors exercised in New Zealand

Updates in interpretation: -

A ‘director’ includes anyone acting in a similar capacity — not just officially appointed directors.

- Even if control is exercised digitally, it may still be considered as taking place in New Zealand, depending on the circumstances.

Trusts: who’s a resident? Trusts aren’t separate taxpayers, so residency of the people behind the trust is key to determining its tax obligations.

Key clarifications: - A trust is classified as foreign if the settlor is not a New Zealand tax resident.

-

A complying trust is based on the tax residency of the trustee(s).

- Having even one NZ-resident trustee (including a corporate trustee) can make the trust a NZ-resident trust.

- NZ-resident trustees of foreign trusts must:

- Register the trust, and

- File annual returns to maintain complying trust status

Questions or concerns? Tax residency rules can be complex and fact-specific. If you’re uncertain how these updates may apply to you or your business, please contact us — we're here to help. |

Tax & Financial Updates – July 2025 |

KiwiSaver Changes -

From 1 July 2025: Government contribution reduced to $0.25 per $1 contributed. Max contribution now $260.72.

- From 1 April 2026: Default contribution rate increases to 3.5% for employees and employers.

-

From 1 April 2028: Rate increases again to 4% for employees and employers.

Residential property interest deductibility

From 1 April 2025, property owners can claim 100% of interest costs on residential investment properties. Home office square metre rate

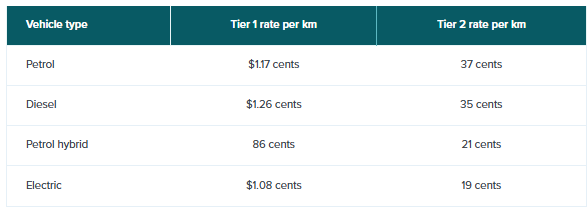

The square metre rate for the 2024–2025 income year is $55.60. Mileage rate

The mileage rates for the 2024- 2025 income year: |

FamilyBoost scheme – key changes

These changes are intended to apply for early childhood education costs incurred in the 1 July to 30 September 2025 quarter onwards: - Income threshold increase: Max eligible household income raised to $229,100 annually.

-

Rebate Increase: Families can claim 40% of ECE costs, up to $1,560 per quarter.

- Slower abatement rate: Reduced to 7% for income over $35,000 per quarter.

|

Payroll enhancements - Redesigned employee profile in Xero Me app for easier updates.

Online payments - Tap to Pay now available on iPhone and Android for faster invoice payments.

Tap to Pay allows the business owner to get invoices paid faster by giving the ability to take payment from customers on the spot. In-App guides - Xero have added helpful in-app guides to the Xero Accounting App to make it even simpler to get set up correctly and master the essentials like invoicing.

- This new guided set-up walks you through the first key steps inside the app so you can start using Xero's powerful features faster.

-

Sending that first invoice is even easier with invoice guide which uses simple on-screen tips to show you exactly how to create and send invoices straight from the app.

-

Xero also added a guide just for configuring your invoices. From logo, business details, payment advice, and tax information - set up your professional-looking template from the app for consistent, sharp invoices every time.

Invoicing improvements - Compact line-item display.

- Inventory dropdown includes first 100 items.

- Ability to add or reorder empty rows.

- Column preferences remembered per invoice.

|

From 1 September 2025, the price of Xero GROW, COMPREHENSIVE and ULTIMATE plans will increase in New Zealand.

Xero is proud to enhance its platform with exciting new features designed to benefit businesses. In the coming months, customers can anticipate a redesigned navigation and dashboard, offering a clearer, at-a-glance understanding of their business's performance.

*all prices are GST exclusive - Xero GROW plan increases from $75* to $83* per month

- Xero COMPREHENSIVE plan increases from $99* to $110* per month - Xero ULTIMATE plan increases from $113* to $125* per month |

Swolefoods: A Kiwi Start-Up Transforming the Way We Eat

|

From humble beginnings in a home kitchen to becoming one of New Zealand’s fastest-growing health food brands, Swolefoods is redefining how Kiwis approach convenient, nutritious eating.

Founded by Taran (Taz) Machra, a passionate health enthusiast with a background in nutrition and fitness, Swolefoods began as a bootstrapped venture driven by a single mission: make clean, high-protein meals more accessible for everyday people. With no outside investment so far and a relentless commitment to quality, Taz turned a personal vision into a business that now delivers thousands of ready-made meals each week across the country.

Today, Swolefoods has become a household name in the world of functional food. Known for its chef-prepared, macro-balanced meals that save time without sacrificing flavour or nutrition, the brand is now shaking up the supermarket aisles with two major innovations: Swolefoods Protein Ice Cream and Swole Cakes – a high-protein pancake mix.

The Protein Ice Cream range combines indulgence with performance – a guilt-free dessert made with no added sugar, low carbs, and over 20g of protein per tub. It's already gaining momentum with stockists like New World, Four Square, Mobil, and Z Energy.

Likewise, Swole Cakes taps into the growing demand for healthier breakfast and snack options. These protein pancake mixes are made with clean ingredients, contain zero added sugar, and deliver serious nutritional value without compromising on taste. They are perfect for families, fitness lovers, and anyone wanting better-for-you food.

As Swolefoods scales, the brand remains deeply grounded in its purpose: to help busy people make better food choices without the stress of planning, prepping, or compromising on taste. With an expanding retail presence, national brand partnerships, and more innovation on the horizon, Swolefoods is a true New Zealand success story, proof that with grit, passion, and purpose, even the smallest ideas can go big. |

|

|