Keep up-to-date with us and what's happening in the business world |

|

|

- 5 Tips for Controlling Your Cashflow - Important Notices - Minimum Wage to Rise From April 1 ($23.95 per hour) - Xero Tip of the Month: Review Your Repeating Bills

- Tax Question of the Month: Early Year-End Preparation: What's the Benefit? - IRD Upcoming Tax Payment Dates |

|

|

Cashflow is the lifeblood of every business. Even profitable companies can run into trouble if money isn’t coming in fast enough to cover day-to-day expenses. Delayed payments from clients, unexpected costs or overstocked inventory can all put pressure on your cash position and that stress can keep even the most experienced business owners up at night.

The good news? With some proactive planning and smart strategies, you can take control of your cashflow and protect your business. Here are five practical tips to help you do just that. 1. Give your accounts receivable a boost Invoice your client as soon as the job is completed, or consider invoicing in instalments once key milestones are reached. Also, make sure you have strict payment terms in place.

2. Negotiate longer payment terms

Talk to your suppliers to negotiate 30 or 60-day payment terms. This delays payment for your most common overheads, helping you spread the cost over a longer period.

3. Always have a cash reserve in place Putting surplus profits into a cash reserve gives you a buffer to draw on when cashflow is challenging. This can be a great way to get through quiet periods or cover unexpected costs.

4. Make the most of your cashflow forecasting tools

Use the cashflow tools in your accounting software or forecasting app to create a rolling cashflow forecast. This helps you spot the potential cash shortfalls and budget accordingly.

5. Keep a close eye on inventory levels Review your inventory levels and warehouse stock to make sure capital is not tied up in slow-moving stock. Think about a leaner approach that reduces your costs. More helpful advice on managing your cashflow:

If your current cashflow position is worrying you, come and talk to our team. We’ll give you tailored advice on how to boost your cash inflows and reduce your cash outflows. Call us today on 04 970 1182. |

|

|

KiwiSaver Contribution Updates (and temporary rate reduction requests)

From the start of the new financial year, 1 April 2026, the default KiwiSaver contribution rate will increase to 3.5% for both employees and employers (up from 3%). It’s a good idea to let your team know about this change and that if they want to keep contributing at 3%, they can apply for a temporary rate reduction now. Employees can choose a reduction period from 3 months up to 12 months, and reapply if needed. Key points for your staff: • Employers can choose to match a temporary rate reduction. • When an employee moves back to the higher rate, IRD will notify you. • This helps employees manage cashflow while continuing to save for the future. Sharing this information now means your team can plan ahead, and your business stays compliant with the KiwiSaver changes. |

MINIMUM WAGE TO RISE FROM APRIL 1 ($23.95 PER HOUR) |

|

|

A reminder that the minimum wage will go up from April 1 2026, to $23.95 - a 3.5% increase from $23.15. The training and starting-out minimum wages will both increase to $19.16 per hour, remaining at 80% of the adult minimum wage. This is a rise from the current minimum rate of $18.80 per hour. Before this change takes effect, it's important to:

- Advise your impacted team members of the increase

- Check your payroll systems and processes

- Update your employment agreements if relevant

- Update your business budget.

|

| |

|

Costs are increasing Even if you don’t employ one of the 175,000 Kiwis who earn minimum wage, this may impact your business. Wages rise steadily over time, and employees who missed out on a pay rise this year will probably expect one next, if your business has been thriving. In addition to the rising cost of labour, inflation is forecast to put upward pressure on everyday items. That will likely increase your general running costs and the price of materials. Petrol prices are up, for instance, and supply chain issues have driven up the cost of many imported products. Time to review your pricing

Is it time to put your prices up? Ideally, your business should increase costs by a tiny amount each year, rather than by a big jump every five years, for instance. Small increases help prevent price shocks for customers, and keep your business in line with the rest of the market.

Can you also cut costs?

If you don’t think increasing your prices is an option, or you still need to make more of a change, you may need to cut back your spending. We look at your business line by line, so we can help you identify areas where you might be able to trim the fat.

Need to review your pricing? Our team are here for you; we have a number of pricing tools available for clients to utilise. Get in touch, we are here to help. |

|

|

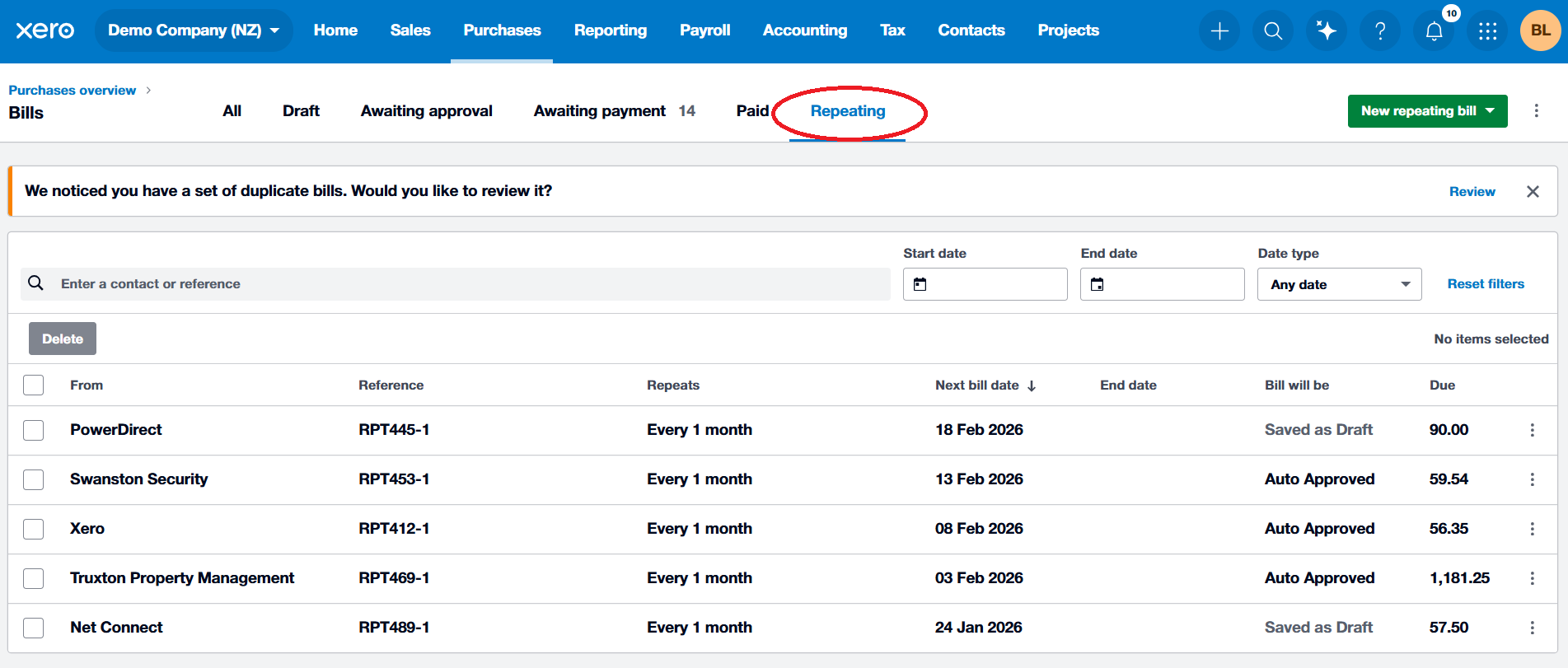

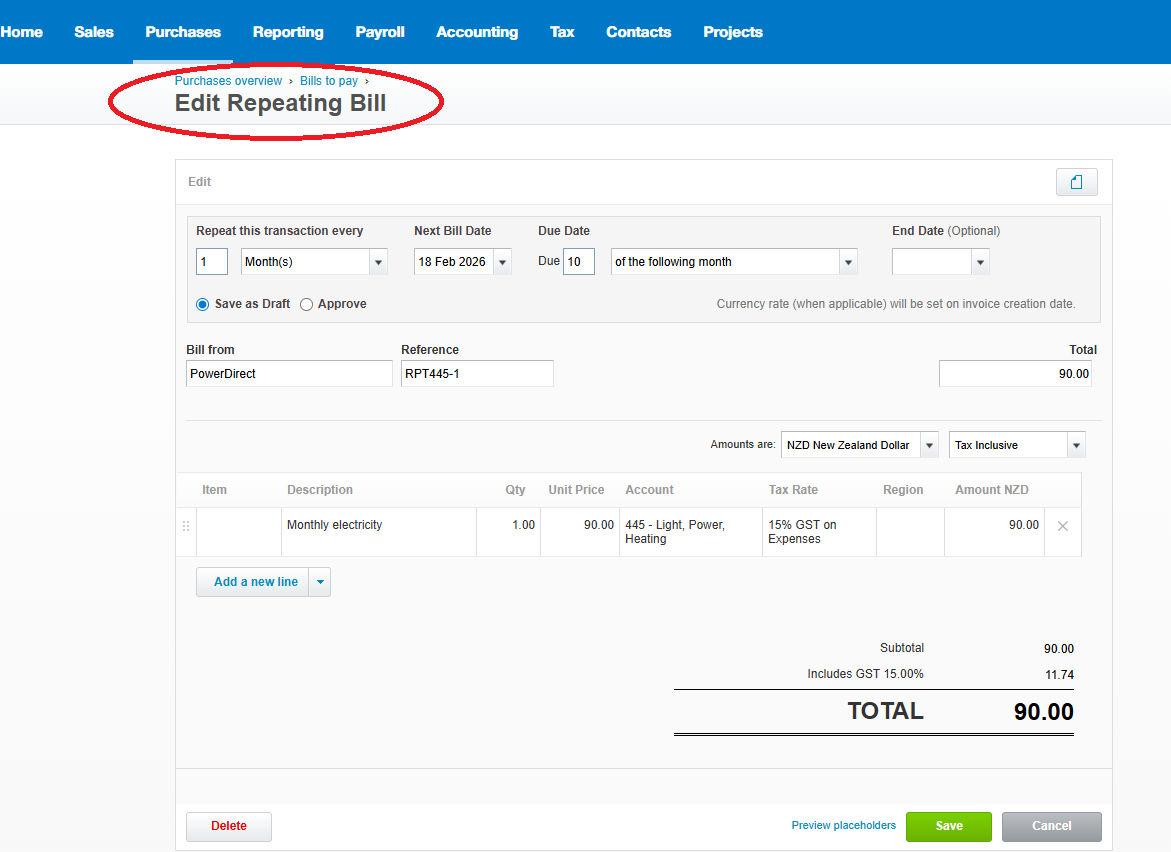

XERO TIP OF THE MONTH: REVIEW YOUR REPEATING BILLS |

At the start of the year, it’s a good idea to review your repeating bills in Xero to ensure they’re still accurate and up to date.

Repeating bills are often created once and then left running in the background. Over time, amounts may change, services may no longer be required, or accounts may need updating. If they aren't reviewed, outdated repeating bills can lead to incorrect expenses and inaccurate reporting early in the year.

Taking a few minutes now to check your repeating bills helps keep your financial information accurate and reduces the need for corrections later. For those who need a reminder, you can find your repeating bills under

Purchases > Bills > Repeating and update or stop any that are no longer needed. |

|

| TAX QUESTION OF THE MONTH: |

QUESTION: Sarah runs a busy marketing consultancy. In early March, she received a standard email from her accounting firm with a checklist, kindly requesting that she start gathering her financial information for the year. Her initial thought was, "Already? The financial year isn't even over yet." Like many business owners, Sarah's focus was on finishing projects for her clients, not on accounting admin. She viewed the year-end process as something that happened after 31 March. Curious about the timing, she called her accountant with a common question: "I've received your request for my year-end information. Why is it so important for me to start this process now, before the financial year has even finished?" |

ANSWER:

Sarah's accountant explained that her question was a good one and that the firm's request was designed to make the entire year-end process smoother and less stressful for everyone involved.

The accountant explained that the goal is to shift from a last-minute rush to a well-planned process. An early start allows the accounting team to work with clients proactively. This approach has several key benefits: -

It Reduces Future Pressure: The period just after 31 March can be hectic for business owners. Gathering documents in March, while the year's events are still fresh, is far easier than trying to recall specific details or locate receipts many months later.

-

It Allows for Early Identification of Issues: When the firm receives information early, the accountants can perform a preliminary review. This often helps to spot missing bank statements, details of a large asset purchase, or unclear transactions. It provides plenty of time to resolve these queries without causing delays down the line.

-

It Creates a Window for Planning: An early review can highlight opportunities for last-minute, legitimate tax planning. For example, it might prompt a discussion about writing off specific bad debts or obsolete stock, actions which must be completed before 31 March to be effective for the current tax year.

-

It Ensures a Smooth Workflow: To meet the filing deadlines set by law, accounting firms manage a carefully planned schedule. When clients provide their information in a timely manner, it helps secure their place in the workflow and ensures their accounts get the full attention they deserve.

|

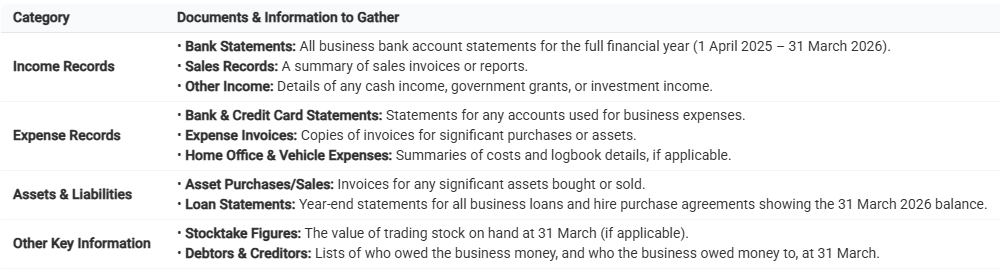

A Practical Checklist for Year-End: To help Sarah get started, her accountant directed her to the checklist of key documents and information. |

The Outcome

After the conversation, Sarah understood the value of the early request. It wasn't just about administrative compliance; it was the first step in an efficient process designed to finalise her accounts accurately and without unnecessary stress.

While a business's tax return is not due to be filed until later, often 7 July for individuals or the following 7 April for those linked with a tax agent, the preparation work begins as soon as the financial year closes. Most businesses operate with a standard balance date of 31 March, which marks the end of their income year. Starting the information-gathering process together in March is the best way to ensure a successful outcome for everyone.

For a comprehensive understanding of your obligations to maintain records and provide correct income information, you can refer to the Tax Administration Act 1994, particularly Part 3. |

References

Tax Administration Act 1994, s 22H |

|

|

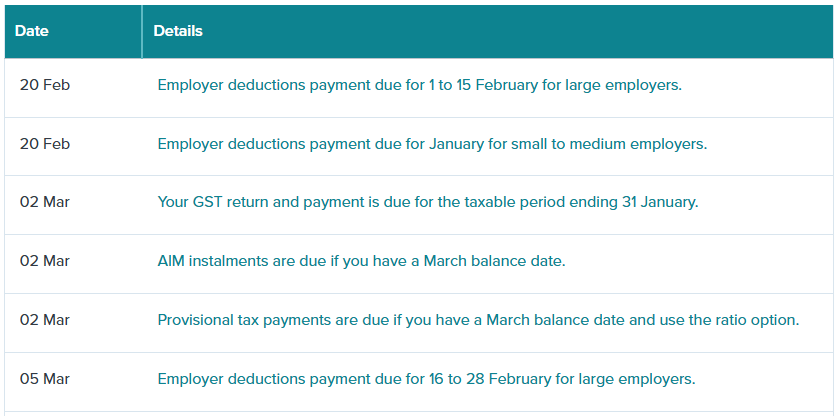

IRD UPCOMING TAX PAYMENT DATES |

|

|

|