Keep up-to-date with us and what's happening in the business world |

|

|

- 2025 Annual Accounts Questionnaires - Important Notices - The Fundamentals of a Business Budget - Xero Tip of the Month: How to Export and Back Up Your Financial Data

- Reminder: KiwiSaver Government Contribution - Are you on track? - Tax Question of the Month: Case Study - Can This Family Claim the FamilyBoost Tax Credit?

- IRD Upcoming Tax Payment Dates |

|

|

As mentioned in our March and April newsletters, we’ve transitioned to a digital format for our End of Financial Year (EOFY) questionnaires. If you’re a business or rental property client, you should have received an email with the link to your online questionnaire(s). If you haven't seen it in your inbox, please check your spam or junk folder—or get in touch with us, and we’ll be happy to resend it.

For clients who require a Personal Accounts Questionnaire, we appreciate your patience. To help us manage workflow volumes more effectively, these questionnaire emails will be distributed progressively throughout June and July. Rest assured, our four-week turnaround guarantee will still apply from the date we receive your completed questionnaire along with all the required documents and information.

If you'd prefer to get started sooner, you’re more than welcome to use the previous system by downloading the questionnaire from our website (Services / 2025 Annual Accounts Questionnaires). If you have any questions, concerns, or encounter any issues, please don’t hesitate to get in touch with our team on 04 970 1182 or email us at admin@aafl.nz — we’re here to help. Important Note: Team Overseeing 2025 Annual Accounts

As we work on preparing your 2025 annual accounts, you may be contacted by a team member at All Accounted For whom you haven't interacted with before. They may get in touch to request additional information needed to progress your accounts.

This is all part of our collaborative approach to ensure the process is as smooth and efficient as possible. Your primary accountant remains your main point of contact and is always available to assist with any questions or concerns throughout the process.

To make things a little easier, we've included a link to our full team below. Simply click the button to access it. Thank you for your continued understanding and cooperation. |

|

|

2025 Government Budget

On Thursday, 22 May 2025, the Government will release the details of the 2025 Budget, titled “The Growth Budget.”

This year’s Budget will focus on driving economic growth and boosting productivity, with the goal of building a stronger, more resilient economy that lifts real incomes and creates greater opportunities for New Zealanders.

It’s also expected to include targeted measures to support small and medium-sized enterprises (SMEs). While direct funding may not be a key focus, the Budget is set to feature initiatives aimed at fostering a more favourable environment for business growth and innovation.

In addition, early announcements suggest the 2025 Budget will build on the 2024 initiatives to address the rising cost of living, enhance health and education services, and restore law and order.

Rest assured, we’ll be reviewing the Budget in detail once it’s released to identify anything that may benefit our clients or pose potential challenges. Keep an eye out for our General Ledger – Budget Special next week for a full breakdown. Reminder: Small Business Cashflow (SBC) Loan Repayments:

We've noticed some recent communications from Inland Revenue regarding the Small Business Cashflow (SBC) Loan, encouraging businesses to avoid default interest by repaying their loans now.

We’d like to remind you that the SBC Loan has a five-year repayment term, starting from the date the funds were first drawn. The loan remains interest-free for the first two years. After that, a 3% interest rate applies, and regular repayments of both principal and interest are required.

To stay on track and avoid any penalties, we recommend checking your loan balance in myIR, making additional repayments if possible, and setting up a repayment plan if needed.

If you have any questions about your loan or repayment schedule, please don’t hesitate to contact us at 04 970 1182. We’re always here to help! |

THE FUNDAMENTALS OF A BUSINESS BUDGET |

|

|

A business budget is one of the essential tools in managing your finances and actively building your business. A budget shows what you plan to do with your cash over the next year.

For a complete picture of your business health, you need to review the profit and loss statement, the balance sheet, the cash flow forecast and the budget. Taken together, these reports allow you to make informed business decisions and monitor performance. |

| |

|

Why have a Budget? - Forecast sales and expenses according to monthly or quarterly variations.

- Evaluate performance over time, including changes or patterns.

-

Get really familiar with where your money goes and where it comes from.

- Clarify targets and goals and use the budget to help you focus and achieve those goals.

- Comparing actual figures to budgeted figures allows you to see potential problems early and plan for unexpected costs.

-

A budget will help you to see the big picture and stay motivated over the long term.

Where to start

A basic budget takes known income and expenses, then makes certain assumptions about the timing of income and planned expenditure. The basic budget is based on cash in and out of the business.

Over time, as you start to see the benefits of using a budget, your budget should evolve into a more sophisticated version that includes non-cash elements such as provisions and depreciation.

Most businesses will start with one budget but soon move to having three budgets: - Business as usual – the next year’s budget is based on current year income and expenses, with perhaps a small adjustment for consumer price index increases.

-

Worst case – budget is based on a pessimistic view of next year’s performance.

- Best case – budget is based on an optimistic view of performance over the next year.

A budget is usually for a financial year, but you can also set up budgets for two to five years.

Once you have one budget (or more) set up, you can then run your current financial reports against the budget to see how you are tracking. This allows you to make rational business decisions in real time to adjust accordingly.

Your can run your financial reports monthly and adjust your budget as needed. What Next?

Now is a great time to put a budget into place for the coming financial year. Book a time with us to help you create a meaningful budget in your accounting software so that you can use it as a proactive part of your business management, strategy and your success. |

|

|

XERO TIP OF THE MONTH: HOW TO EXPORT AND BACK UP YOUR FINANCIAL DATA |

When it comes to your financial data, you can never be too cautious! While Xero is a cloud-based platform with strong security measures, it’s always a good idea to back up your financial data regularly for peace of mind. Regular exports of important reports and transactions can serve as a safeguard against any unforeseen issues. Although Xero doesn't have a built-in backup feature, you can manually export your data to store it on your local device or secure cloud storage. Alternatively, you can use third-party apps to back up your Xero data, such as:

Coupler.io: This app automatically exports data from Xero to spreadsheets, data warehouses, and BI tools. You can set the refresh interval to daily, monthly, every hour, every 30 minutes, or every 15 minutes.

Xportmydata: This app automatically backs up your Xero data on a weekly basis. You can also use Xportmydata to export your Xero data to Excel, download attachments, and create CSV import files.

Both of these apps are available for download from the Xero App Marketplace. Manual Exporting:

If you prefer to export your data manually, Xero doesn’t have a feature to copy all your school's data at once. However, you can export data from specific sections and generate reports individually. Your ability to export data depends on your user role in Xero. If you have the adviser role, you can run and export most reports. However, to export payroll reports, you need payroll admin access. To learn more about how to export your data manually, click the button below. |

|

|

REMINDER: KIWISAVER GOVERNMENT CONTRIBUTION - ARE YOU ON TRACK? |

Time is ticking! With just over six weeks left until the deadline, now is the time to check that you're on track to receive the KiwiSaver Government contribution of $521.43.

To qualify for the full contribution, you must: -be a Kiwisaver member -live in New Zealand -be 18 years old or younger than 65 -have contributed a least $1,042.86 to your KiwiSaver account by 30 June 2025. If you're falling short, a one-off payment could help you meet the threshold and qualify for the government contribution. You can find more information on the Inland Revenue website by clicking the button below. |

|

|

TAX QUESTION OF THE MONTH:

|

A New Zealand couple, both tax residents, want to know if they can claim the new FamilyBoost tax credit for the early childhood education (ECE) fees they paid in the 2025 tax year. Their 4-year-old child attends a licensed ECE provider.

Here’s a summary of their situation: - The husband is a shareholder-employee in his own company and earns:

$70,000 in salary (with PAYE deducted)

$100,000 in dividends from the company (received in the last quarter of the year) - The wife earns $30,000 in PAYE wages from a completely separate employer.

QUESTION 1: ARE THEY ELIGIBLE FOR FAMILYBOOST? ANSWER: The FamilyBoost tax credit was introduced in 2024 and is available from 1 July 2024. To qualify, a person must meet four key criteria: - They’re the caregiver of a child aged 5 or under

- They’re paying fees to a licensed ECE provider

- They are a New Zealand tax resident

- Their household income is less than $45,000 per quarter

In this case, the couple meets the first three criteria. The key question is whether their combined quarterly income stays under $45,000. Let’s break it down:

For the two quarters from 1 July 2024 to 31 December 2024: Combined income = $70,000 + $30,000 = $100,000

Divided evenly over 4 quarters = $25,000 per quarter ✅ Eligible (under the $45,000 threshold)

For the last quarter (1 Jan – 31 Mar 2025): The husband receives his $100,000 dividend

Total income for the quarter = $17,500 (his salary) + $7,500 (her salary) + $100,000 (dividend) = $125,000 ❌ Not eligible (over the $45,000 threshold) Summary:

They qualify for FamilyBoost for two quarters (July to December 2024) but not for the last quarter when the dividend was paid.

QUESTION 2: WHAT IF THE HUSBAND’S SALARY DIDN’T HAVE PAYE DEDUCTED? ANSWER:

If the husband’s salary wasn’t paid through PAYE, it changes how income is assessed: -

Without PAYE, the income is not “reportable” (IE: income the IRD automatically receives info on)

- In that case, his income for FamilyBoost purposes is calculated as 25% of his total annual taxable income, based on his most recent tax return

-

If he earns both reportable and non-reportable income in a quarter (like a dividend and a non-PAYE salary), IRD will use whichever amount is higher to assess eligibility

Key takeaway:

To maximise eligibility, it’s best that shareholder-employee salaries are paid with PAYE deducted. References

Income Tax Act 2007 subpart MH

Tax Administration Act 1994 s 22D(3) |

|

|

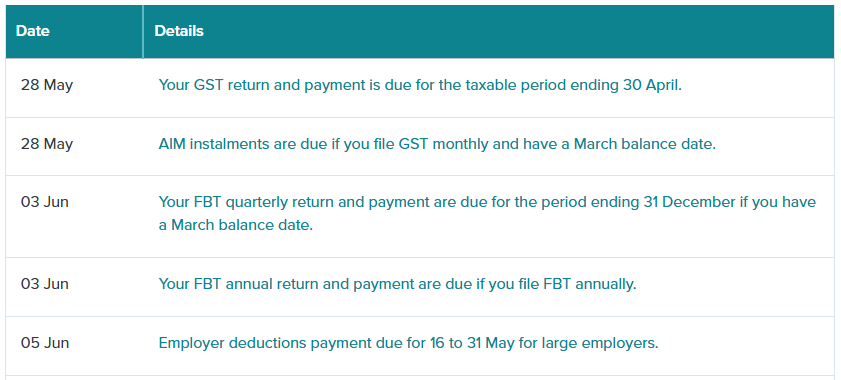

IRD UPCOMING TAX PAYMENT DATES |

|

|

|