Keep up-to-date with us and what's happening in the business world |

|

|

- 2026 Annual Accounts Questionnaires - Terminal Tax Reminder - Due 7 April 2026 - Important Payroll Changes Effective 1 April 2026 - Xero Tip of the Month: Review Archived Accounts Before Year-End

- Tax Question of the Month: Shareholder Salaries vs. Drawings - IRD Upcoming Tax Payment Dates |

|

|

The end of the financial year is fast approaching, and it’s time to start preparing your annual accounts. To make this process as smooth and efficient as possible, we’ll be sending your End of Financial Year Questionnaire(s) via email in the same format as last year.

These questionnaires are an important part of the year-end process, helping us gather all the information needed to prepare your accounts accurately and efficiently. Completing and returning your questionnaire promptly ensures we can finalise your accounts and tax returns without delays. You can expect to receive your questionnaire(s) between April and May, giving you plenty of time to gather any necessary information.

For anyone who may have difficulty using the online system, the previous format is still available. Downloadable versions of the questionnaires can be accessed via our website under Services / 2026 Annual Accounts Questionnaires.

If you have any questions or need assistance, our team is always happy to help.

Step-by-Step Guide for Completing Your Digital Questionnaire -

Check your inbox: You will receive a secure email from All Accounted For containing a link to your personalised questionnaire(s). If our email address is not saved as a contact, the email may end up in your spam or junk folder, so please check there if needed.

-

Complete the questionnaire: Please complete the questionnaire at your earliest convenience and ensure all sections are filled out accurately. The sooner we receive your information, the sooner we can complete your accounts and tax returns.

-

Provide complete and accurate information: Ensure all information provided is accurate and complete to avoid follow-ups or delays.

- Submit your completed questionnaire(s): Once completed and all necessary documents are attached, simply click “Submit.” We will be notified immediately and can begin reviewing your information.

|

|

|

TERMINAL TAX REMINDER - DUE 7 APRIL 2026 |

Just a reminder that your terminal tax payment is due on Monday, 7 April 2026. We will be sending out terminal tax reminder letters via email in the next couple of weeks. Please ensure that your payment is made on or before the deadline to avoid any penalties or interest charges. If you have any difficultly making the payment in full, please contact us as soon as possible (admin@aafl.nz or 04-970-1182) to discuss options, such as instalment arrangements or deferring through Tax Management NZ. |

|

|

IMPORTANT PAYROLL CHANGES EFFECTIVE 1 APRIL 2026 |

As an employer, it’s important to stay informed about upcoming changes that affect payroll, employee entitlements, and contributions. From 1 April 2026, there are several key updates to the minimum wage, ACC Earner Levy, and KiwiSaver contribution rates.

Below is a summary of these changes and what they mean for you and your business, including the actions you may need to take to ensure compliance and manage the impact on your payroll and cashflow. |

| |

|

1. Minimum Wage Increase: - The Adult Minimum wage is increasing from $23.50 per hour to $23.95 per hour

- The Training and Starting-Out Minimum wages are increasing from $18.80 per hour to $19.16 per hour

What this means for you: If you have any employees on Minimum Wage you will need to ensure their pay rate is updated from 1 April 2026. Also check any salaried employees meet minimum wage requirements by taking salary divided by actual hours worked. For someone on salary that is close to minimum wage, this is a check that is required each pay if irregular hours are worked. 2. ACC Earner Levy Increase: The ACC Earner Levy rate is increasing from $1.67 to $1.75 per $100 of liable earnings. These amounts are inclusive of GST. The maximum liable earnings threshold increases to $156,641.

What this means for you: Your payroll software should automatically update (but it always pays to check with the software team). Your employees may notice a small change (reduction) in their take home pay due to this change. 3. KiwiSaver Contribution Changes

The minimum / default KiwiSaver contribution rate is increasing from 3% to 3.5%. This relates to both Employer contributions and Employee contributions.

Temporary Rate Reduction: Employees can apply for a temporary rate reduction from 1st February 2026 if they want to carry on contributing at 3% from 1st April 2026. They can apply for the temporary rate reduction for a 3 month to 12 month period, and they can apply as many times as they like. The Temporary Rate reduction can be applied for through their myIR account. More details can be found here

Employers can choose to match the Employees temporary rate reduction, moving the Employer contributions down to 3% to match, but they can also choose to stay contributing at 3.5%. What this means for you: Again this change will impact on your wage expenses, so check in on your cashflow planning and how this may impact.

Future planning: From 1st April 2028 the minimum/default KiwiSaver contribution rate will increase again to 4% |

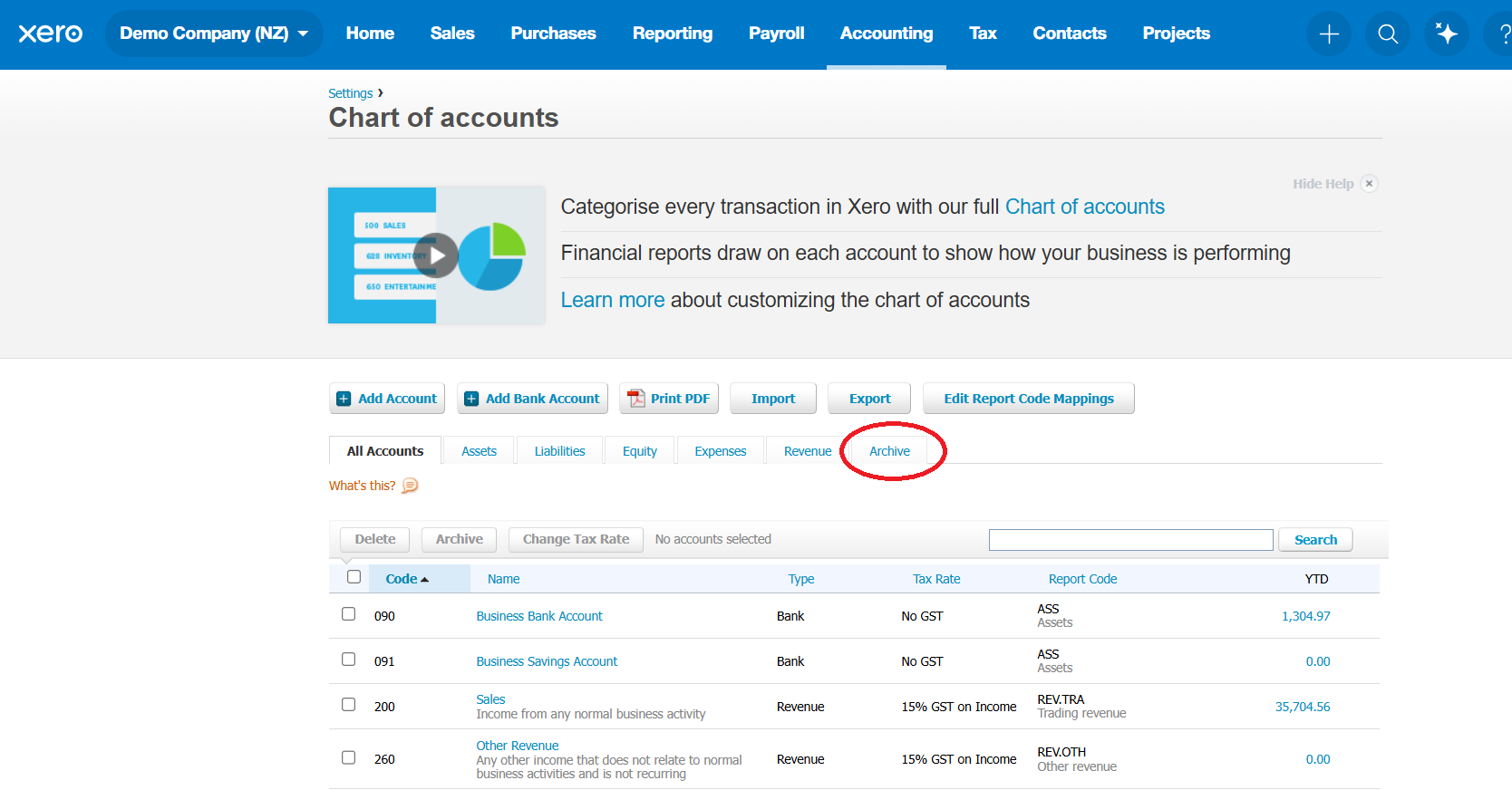

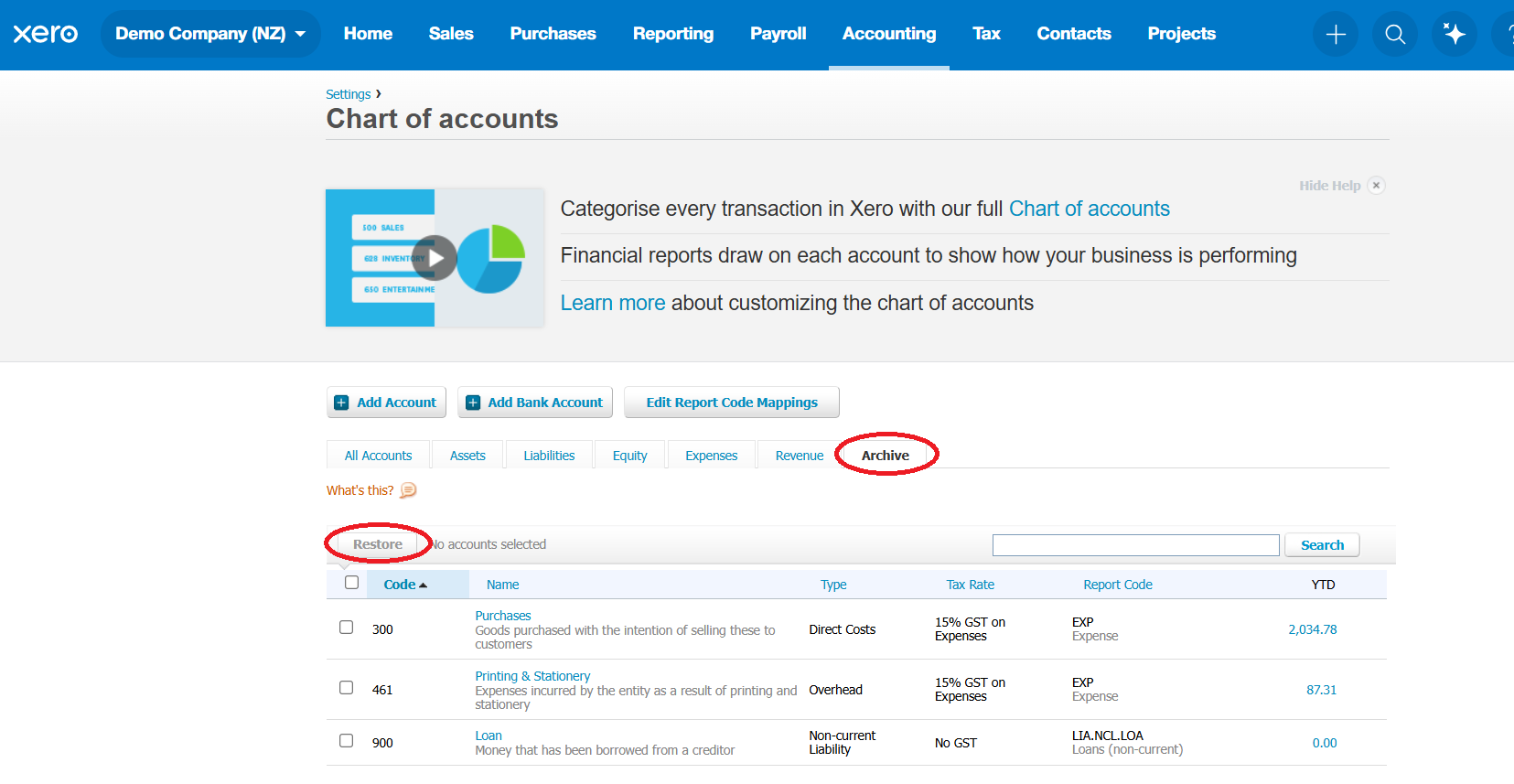

XERO TIP OF THE MONTH: REVIEW ARCHIVED ACCOUNTS BEFORE YEAR-END |

Archived accounts in Xero help keep your Chart of Accounts tidy, but they still retain balances and appear in historical reports. If overlooked, they can quietly create discrepancies in your Profit & Loss or Balance Sheet.

Regularly reviewing archived accounts ensures all balances are intentional and coded correctly, giving you confidence in your reporting and helping year-end processes run smoothly. How to review archived accounts in Xero: -

Go to Accounting → Chart of Accounts.

- Click the Archive tab to view archived accounts.

- Check for any balances or transactions.

-

Unarchive accounts if adjustments are needed, then re-archive once correct.

A quick monthly check helps prevent surprises and keeps your financial reporting accurate, reliable, and stress-free. |

|

|

TAX QUESTION OF THE MONTH: |

QUESTION:

A director of a small owner-operated company has been taking regular payments from the business account to cover personal living costs. They are seeking clarity on the difference between treating these as drawings versus a shareholder salary, and what actions must be taken before 31 March. |

ANSWER:

This is one of the most important concepts for a company owner to understand. The distinction between "drawings" and a "shareholder salary" is critical, as they have vastly different tax and legal implications. Incorrect treatment can lead to unexpected tax bills and compliance issues.

The Fundamental Difference: Company vs. Shareholder

The first step is to remember that under New Zealand law, a company is a separate legal entity from its shareholders. -

The company earns the business income and pays tax on its profits at the company tax rate (currently 28%).

- The shareholder is a separate taxpayer.

Any money taken from the company by its owner must be properly categorised. It cannot simply be an informal withdrawal. Drawings (Shareholder Loan Account)

When a shareholder takes "drawings," they are effectively borrowing money from the company. These payments are not a business expense and are not tax-deductible for the company. Instead, they create a debt that the shareholder owes back to the company. This is tracked in the Shareholder Loan Account on the company's balance sheet. Key Implications: - No PAYE: The company does not deduct PAYE from these payments.

- Not a Business Expense: The company gets no tax deduction for the amounts taken.

-

Risk of Deemed Dividend: If a shareholder loan account is overdrawn at the end of the financial year (meaning the shareholder owes the company money), this can trigger tax consequences. If the loan is not repaid or formalised with interest charged at the prescribed rate, it may be treated as a dividend, with tax payable by the shareholder personally.

Drawings are essentially a temporary funding mechanism, not a method for remunerating a shareholder for their work.

Shareholder Salary

A shareholder salary is formal remuneration paid to a shareholder for the work they perform for the company. It is treated the same as a salary paid to any other employee.

Key Implications - Company Tax Deduction: The salary is a deductible expense for the company under the general permission (s DA 1, Income Tax Act 2007), reducing the company's taxable profit.

- PAYE Obligation: The company must register as an employer, deduct PAYE from the salary, and pay it to Inland Revenue.

-

Personal Income: The gross salary is assessable income for the shareholder personally.

Paying a salary is the correct way to remunerate a shareholder for their labour and expertise, allowing the company to claim a tax deduction for that cost. Action Required Before 31 March

For a shareholder salary to be a valid deductible expense for the company in the current financial year, it must be properly authorised and documented. -

Quantify the Salary: Determine a commercially realistic salary for the work performed throughout the year. This should be justifiable based on the shareholder's role, hours, and responsibilities.

-

Board Resolution: The company's directors must pass a formal resolution to approve and authorise the salary amount. This resolution must be dated on or before 31 March.

-

Journal Entry: An accounting journal is then passed to record the salary as an expense in the company's books and credit it to the shareholder's loan account.

|

How this Works in Practice:

The salary that has been formally approved via the resolution can be used to "clear" the drawings taken during the year. -

Example: A shareholder has taken $80,000 in drawings. Before 31 March, the company board resolves to pay that shareholder a salary of $80,000 (plus PAYE).

-

Result: The $80,000 salary is a tax-deductible expense for the company. This amount is credited to the shareholder's loan account, which offsets the $80,000 in drawings, leaving the account with a nil balance. The company must then account for the PAYE on that salary.

Failing to pass this resolution before 31 March means the company loses the ability to claim a tax deduction for the shareholder's salary in this financial year. This could result in the company paying 28% tax on profit that should have been paid out as a deductible salary. |

References

For specific rules regarding deductions for employee remuneration and the treatment of shareholder transactions, you can refer to Part D and Subpart CD of the Income Tax Act 2007. |

|

|

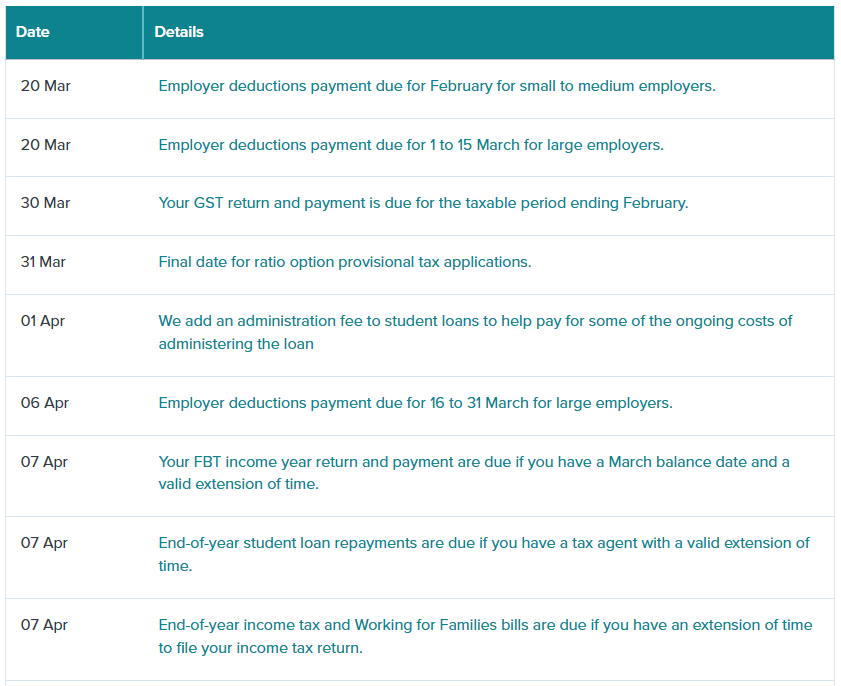

IRD UPCOMING TAX PAYMENT DATES |

|

|

|