Keep up-to-date with us and what's happening in the business world |

|

|

- Tax Planning Helps You Do More With Your Money

- Important Notices - Resource: New Xero Insights Report and Guidance on Small Business Productivity

- Xero Tip of the Month: How to Customise Your Dashboard in Xero - Tax Question of the Month: Cash Incentive to Take out Loan - Income Tax and GST Treatment

- IRD Upcoming Tax Payment Dates |

|

|

Tax planning is a strategic approach to managing your business’ financial affairs, with the aim of legally minimising your tax liability. In other words, you plan ahead to make sure you pay the taxes you should be paying, but not a penny more.

Working with your tax adviser, you can look for deductions, credits, exemptions and tax-saving strategies that will help to optimise your company’s overall tax position. How does tax planning affect your business? The primary goal of tax planning is to reduce the amount of taxes your business owes. But it’s also about making sure you stay compliant with all the tax laws and regulations applicable to your business.

But what are the main advantages? Let’s take a look at five of the big benefits of careful, strategic tax planning. By planning your tax across the year, you can: -

Maximise your profits – strategic tax planning helps your company find the best available tax incentives, deductions and credits. This reduces your overall tax liability, cuts your annual tax costs and increases your overall profitability as a business.

-

Boost your cashflow – tax planning is a great way to open up more liquid cash and achieve a better cashflow position for the business. When you cut down the company’s tax payments, that frees up cash and helps you achieve a positive cashflow position.

-

Stay compliant and mitigate your risk – being proactive with your tax planning keeps the company compliant with the relevant tax laws and regulations. It’s a sensible way to tick the compliance boxes and reduce the risk of costly penalties and legal issues.

-

Drive your strategic growth – smart use of tax planning helps you reduce your tax costs and reassign those funds to your strategic business goals. It’s a golden opportunity to invest in areas that promote long-term growth and competitiveness.

-

Give your business a competitive edge – if managed well, efficient tax planning leads to lower operational costs for the business. This gives you a competitive edge when it comes to pricing, innovation, sales and revenue generation.

How can our firm help you with tax planning?

Getting strategic with your tax planning has many advantages for your financial stability as a business. But to maximise your planning, it’s important to work with an experienced adviser.

As your tax adviser, we’ll help you look ahead across the whole financial year, looking for the opportunities to reduce your tax liability and find the best tax deductions and incentives. If you’d like to know more about the impact of tax planning, we’ll be happy to explain. Get in touch to talk about tax planning today on 04 970 1182. |

|

|

IRD Following Up on Outstanding Unpaid Tax Debt

In the coming months, the Inland Revenue will actively pursue businesses with significant unpaid tax debts who have not yet responded to the multiple notices sent to them. Throughout the pandemic, the IRD has focused its efforts on supporting and assisting small businesses during this challenging period, showing leniency towards many unpaid debts. However, the IRD has announced that they will now be investigating and following up on these cases to ensure compliance. They advise that while payment is necessary, various options are available to assist customers facing financial difficulties.

Therefore, we want to remind you that if you have any overdue debt that is not currently under arrangement, it is crucial that you contact us as soon as possible. By doing so, we can work with the Inland Revenue on your behalf to arrange a payment plan, helping you avoid any potential penalty fees.

|

Bright - line Property Rule: A quick reminder that the New Zealand bright-line property rule has changed as of July 1, 2024.

What does this mean for property owners? -

If you sell an investment property on or after 1 July 2024, the bright-line property rule will only apply if the property is sold within 2 years of purchase. This timeframe has been reduced from the original 5 and 10 year periods.

-

If the property is sold within the 2 year period from date of purchase, any profits will be subject to tax which is calculated by subtracting the purchase price and allowable costs from the selling price.

-

If you have sold a property before 1 July 2024, the original bright-line rule (prior to this change) will still apply, and these rules can vary depending on when you purchased the property.

If you would like to discuss this further or have any questions about how this may affect you, get in touch with us today on 04 970 1182. For more information, please visit the IRD website by clicking the button below. |

New Personal Income Tax Thresholds:

As mentioned in our recent General Ledger 'Budget Special', changes to personal income tax are coming as part of the Government’s Tax Relief package. More information, including a calculator to estimate how much you could benefit, can be found at www.budget.govt.nz

These changes will come into effect from Wednesday, 31 July 2024. Here are the highlights of the upcoming changes:

1. New personal income tax thresholds, shown in the table below. 2. The Independent Earner Tax Credit (IETC) upper threshold for eligibility has been extended from $48,000 to $70,000 3. The base rate for the In-Work Tax Credit (IWTC) will increase from $3,770 ($72.50 per week) to $5070 ($97.50 per week) 4. The after-tax threshold for the Minimum Family Tax Credit (MFTC) will increase from $35,204 to $35,316 |

If you have any questions around the above or would like to chat with our team on how these changes will affect you, please give us a call on 04 970 1182. |

RESOURCE: NEW XERO INSIGHTS REPORT AND GUIDANCE ON SMALL BUSINESS PRODUCTIVITY |

|

|

Looking to boost productivity in your small business without working longer hours?

Discover invaluable insights from the latest Xero Small Business Insights report, "Small business productivity: Trends, implications and strategies", which examines recent productivity trends in Australia, New Zealand, and the United Kingdom.

In addition to trends and insights, this report also provides some tips on how you can increase productivity in your business. You'll find strategies that can be easily implemented to make a significant impact. |

| |

|

To access the full report, click the button below. |

|

|

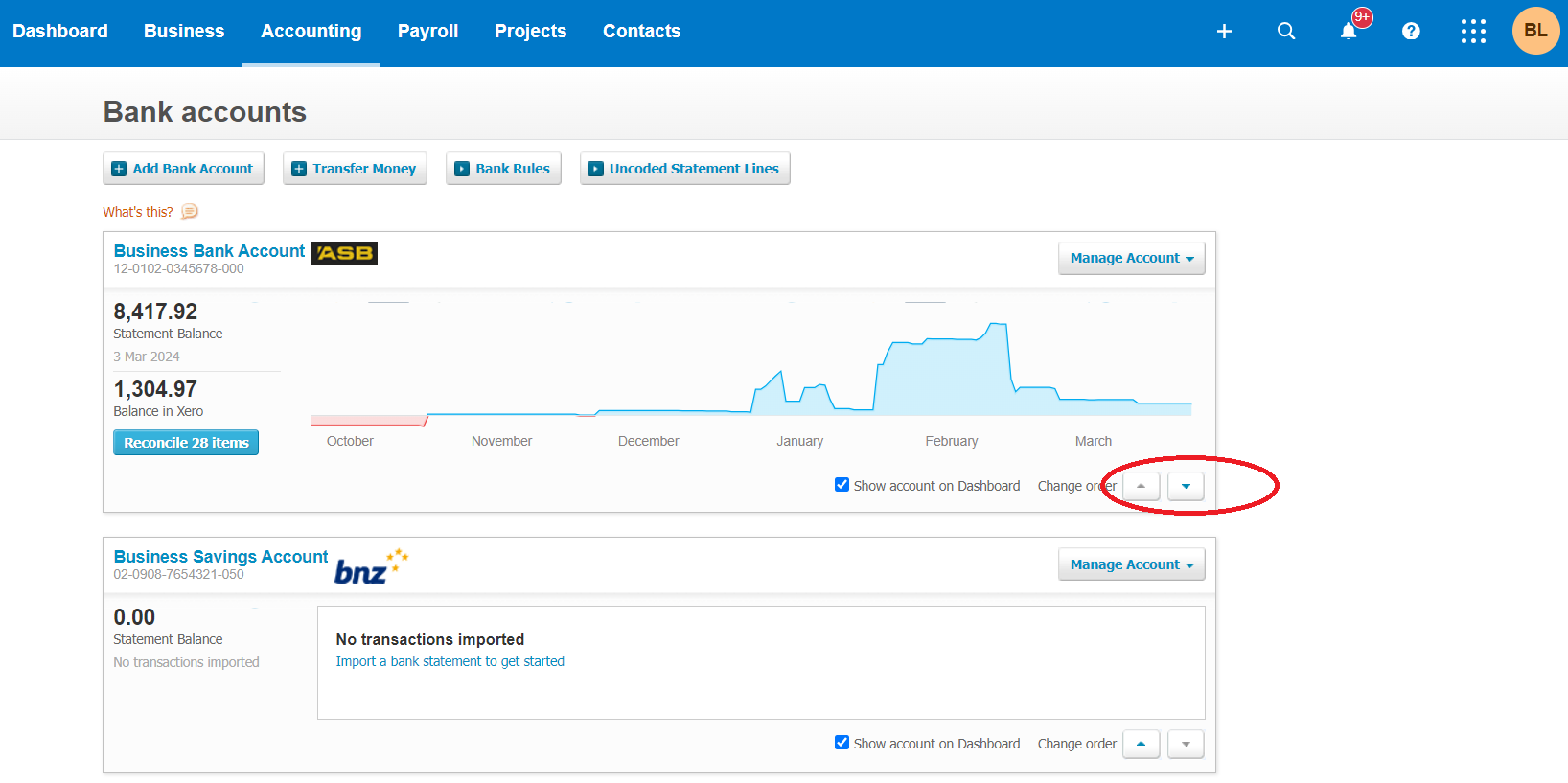

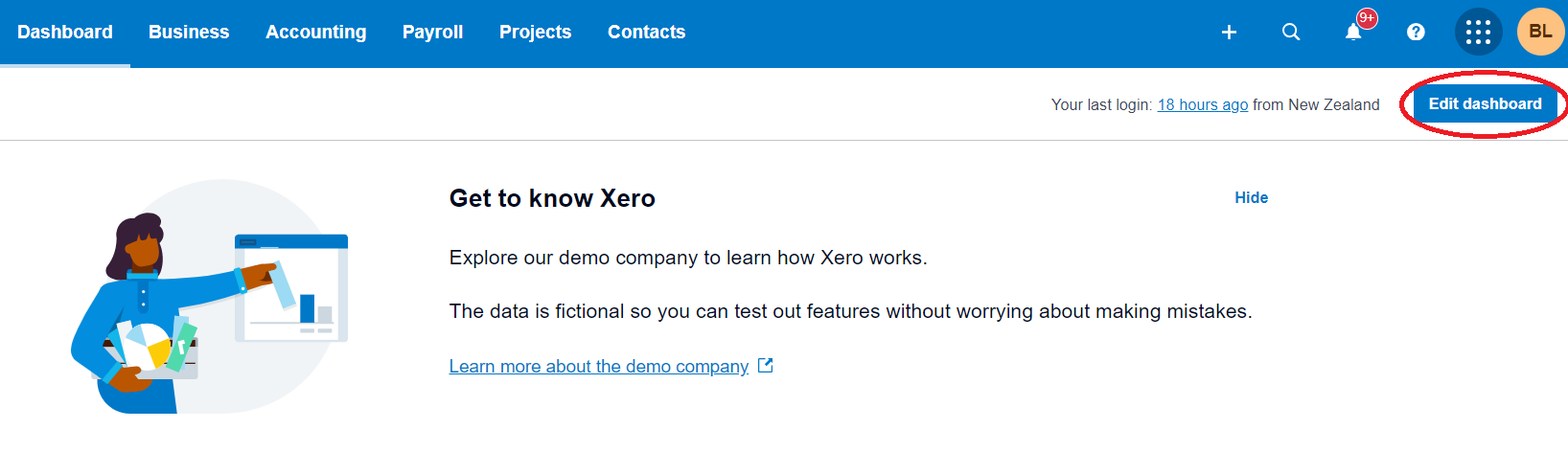

XERO TIP OF THE MONTH: HOW TO CUSTOMISE YOUR DASHBOARD IN XERO |

Did you know you can customise your Xero Dashboard? With the 'Edit Dashboard' feature, you can easily rearrange or remove irrelevant tiles.

To edit the tiles on the Dashboard, click ‘Edit Dashboard’ in the top right corner. From there, drag items to your preferred position or select “Hide” or “Show” to adjust visibility. In addition to this, you can also reorder your school's bank accounts so that the ones you use the most are at the top. To do this go to 'Accounting' - 'Bank Accounts' and use the arrows on the bottom right hand corner to move the accounts up and down. |

|

|

TAX QUESTION OF THE MONTH: |

QUESTION:

Bank B is providing a cash incentive to a borrower for transferring their loan from Bank A to Bank B. The borrower would not have received the incentive had they not agreed to enter into the loan agreement with Bank B.

When a cash incentive is received for transferring a loan to another bank, how is this treated for income tax and GST purposes? ANSWER:

The bank loan is a financial arrangement for tax purposes, so the financial arrangement rules should apply. Assuming that the receipt of the cash incentive was contingent on the borrower entering into the loan agreement, the incentive will form part of the consideration paid to the person under the financial arrangement.

Under the financial arrangement rules, a person will either be a cash basis or a non-cash basis person. A cash basis person is not required to apply a spreading method to income or expenditure under the financial arrangement rules and can instead return income on a cash or "as received" basis. They are still required to undertake a base price adjustment (BPA) calculation when the financial arrangement matures or is otherwise disposed of. To be a cash basis person, the difference between the accrual and cash treatments cannot exceed $40,000 for the income year, and: -

income and expenditure under all financial arrangements for the income year does not exceed $100,000, or

- the absolute value of all financial arrangements does not exceed $1,000,000.

If the person meets the above criteria and is a cash basis person under the financial arrangement rules, they must return the funds as assessable income, which will be taxable to the borrower in the income year in which it is received.

If the person is a non-cash basis person, the funds will be spread over the term of the loan using an acceptable spreading method. We note that a non-cash basis person is also required to undertake a BPA calculation when the financial arrangement matures or is otherwise disposed of.

GST will not be applicable to the cash incentive as it is not a supply of goods or services. It is money, which is not subject to GST. |

|

|

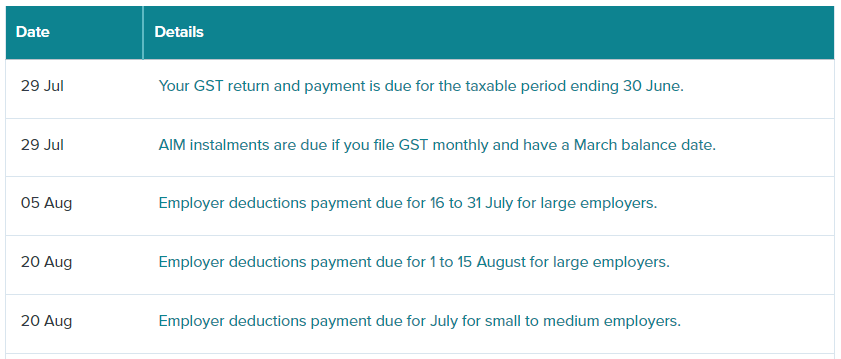

IRD UPCOMING TAX PAYMENT DATES |

|

|

|