Keep up-to-date with us and what's happening in the business world |

|

|

- Merry Christmas & AAF Out-Of-Office Dates - Financial Preparations for the Holidays - Provisional Tax & GST - Due 15 January 2024 - Xero Tip of the Month: Xero Assistance Programme (XAP) - App Spotlight: CoGo - Tax Question of the Month: Family trust making charitable donations

- IRD Upcoming Tax Payment Dates |

|

|

With only a few days remaining until the end of the year, we would like to take this opportunity to express our gratitude for your continued support. We genuinely value the trust you place in us and are proud to be a part of your financial journey.

Looking forward, our team remains optimistic about the future and is committed to delivering exceptional service and innovative solutions. As we close this chapter and welcome a new year, we acknowledge that uncertainties related to government changes and the road ahead may cause unease for some. However, we want to assure you that we are here, ready to support and guide your business at every step of the way. The team at All Accounted For will be taking a much-needed break over the Christmas and New Year period, with our office closing at 12pm on Friday, 22 December 2023, and reopening at 8:30am on Monday, 15 January 2024. On behalf of the entire team at All Accounted For, we would like to wish you a very happy and safe Christmas. We look forward to working with you all in 2024. |

FINANCIAL PREPARATIONS FOR THE HOLIDAYS |

|

|

Now is the time to start planning for your upcoming payments and expenses over the holiday period. To make your preparation a little easier, we have put together a short to-do list below. Whether your business is closed for the holidays or operating throughout, with a bit of planning underway, you should be able to ease into 2024 smoothly, allowing yourself a bit of extra time to enjoy the holiday season. |

| |

|

- Create a staff roster to manage staff leave over the holiday season, making a note of when each staff member will be working and when they are taking a break so you've got enough hands on deck over the holiday period.

-

Pay any outstanding invoices or upcoming invoices.

- Plan for your upcoming tax payment obligations.

- Schedule your staff pay runs if you aren't able to do it on the day.

- Send out your invoices early - this will allow you and your client to have your accounts sorted before you close.

Review your work in progress (WIP) - plan to complete jobs or services that can be invoiced and paid (remember if you don’t invoice and get paid before the break, you may not see the money for another month).

Stock-take - Do you need to order in goods now to be able to complete work in progress? Check that there is stock on hand available. - Plan your 2024 goals: Your review of 2023 goals will give you a good insight into your next steps heading into 2024, so now is the time to write them down.

We can help:

If you’re struggling with your finances and need assistance to tie up any loose ends and answer any queries you may have, All Accounted For can help. We have a talented, highly knowledgeable team of professionals ready to assist you. Get in touch with our team today on 04-970-1182 so we can make your holidays as stress-free as possible. |

PROVISIONAL TAX & GST - DUE 15 JANUARY 2024 |

We have sent the majority of the provisional tax payment reminder letters relating to the second provisional tax amount for the year ended 31 March 2024, which is due 15 January 2024. If you were expecting a provisional tax reminder and have not received one, or if you have any questions around the payment reminder letter received, please contact the team (admin@aafl.nz or 04-970-1182). Also a reminder that GST for the period ended 30 November 2023 is also due 15 January 2024. Again we have sent out the majority of the GST returns for November 2023, with the final few to be sent this week. So make sure you factor in the cashflow required for both taxes and for staff wages through the festive season. If you need an instalment arrangement or extension put in place for the provisional tax or GST, please contact us this week. |

XERO TIP OF THE MONTH: XERO ASSISTANCE PROGRAMME (XAP) |

While there are many moments of the festive season to savor and enjoy, Christmas can also be a busy and stressful time for many. That's why the Xero Assistance Programme (XAP) can be a real game-changer, offering valuable support to help you find balance and take charge of your well-being.

The Xero Assistance Programme, provided through Xero’s partner, Benestar, offers free and confidential well-being support. Whether you're on a starter, standard, or premium plan, you can access this mental health support for free. It's also available to your staff members and their families.

To learn more about the XAP Programme, click the button below. |

|

|

Is your business looking to enhance its sustainability efforts and decrease its carbon impact but uncertain about how to get started? Introducing CoGo NZ, an easy-to-use app that effortlessly helps you measure, track, calculate, and understand your carbon footprint.

This exceptional tool not only identifies your environmental impact but also offers practical, positive steps on how to reduce it, including options for offsetting it entirely. CoGo seamlessly integrates with Xero, linking to your business' Xero file to determine your annual carbon emissions, so it doesn't require any input. |

| |

|

What we love most about this app is that there's no expectation to make unrealistic changes. It simply helps you to see what impact your purchases are having and empowers you to make small changes that could start to make a big difference.

CoGo is now available on the Xero App Store in NZ and the base version is free to use for those runing Xero business editions. To find out more about the CoGo app click the button below. |

TAX QUESTION OF THE MONTH: |

QUESTION:

A company can claim a tax deduction for a donation to a New Zealand registered charity as a business expense and individuals can claim a donation tax credit. A complying trust has investment and rental income and pays income tax, so can the trust claim a deduction for a donation made to a registered charity as an expense against its income? If the answer to the above is yes, if donations exceed income in any one year (resulting in a loss), can this loss be carried forward to the next tax year?

ANSWER:

Generally, an item of expenditure requires a nexus or connection with earning income to be a deductible expense (this is the general permission contained in s DA 1 of the Income Tax Act 2007). A donation to a charity will inherently have no nexus with income as it is not incurred in deriving income or carrying on a business to derive income. Therefore, a donation will not satisfy the general permission.

Section DB 41 specifically allows a company to claim a deduction for certain donations. Any deduction is limited to the company’s net income. So, a loss cannot arise from the donation. However, s DB 41 does not apply to individuals or trusts.

Individuals are entitled to a tax credit for charitable donations under s LD 1. However, s LD 2 provides trusts are not eligible to receive the charitable donation tax credit that individuals can claim.

Accordingly, there is no provision that enables a trust to claim either a deduction or a tax credit for a charitable donation. This aligns with trust law where the trustees must always exercise their powers in utmost good faith for the benefit of the beneficiaries. If the charity is not a beneficiary, then trustees have no power to make a donation.

The trustees may decide to distribute to a charity that is a beneficiary of the trust or comes within a class of beneficiaries of the trust if this is allowed by the trust deed. In this case, provided the distribution to the charity satisfies the criteria to be beneficiary income, the amount of income distributed to the charity will be excluded from the trustee's income and will not be subject to tax in the hands of the trustee. Assuming the charity is a tax charity and meets the requirements for its income to be exempt income under either s CW 41 or s CW 42, the beneficiary income distribution will be tax exempt in the hands of the charity.

|

|

|

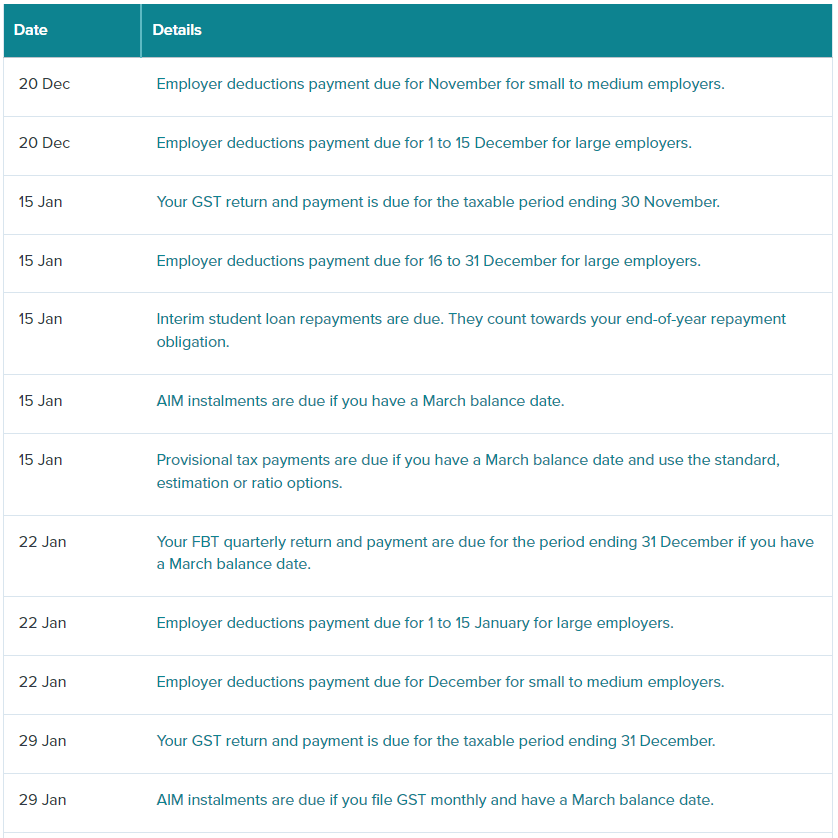

IRD UPCOMING TAX PAYMENT DATES |

|

|

|