Keep up-to-date with us and what's happening in the business world |

|

|

- 2024 Annual Accounts Questionnaires

- Goal-Setting for the New Financial Year: Planning for Success - Inland Revenue Important Notices - New GST Rules Affecting Short-Stay Accommodation Providers - Xero: Classic Invoicing Is Retiring - 2 September 2024 - Xero Tip of the Month: Retrieve Deleted or Voided Bills

- Tax Question of the Month: Is Expenditure on Newly Purchased Earthquake-Damaged Rental Property Deductible?

- IRD Upcoming Tax Payment Dates |

|

|

A reminder that the 2024 end of financial year questionnaires can be accessed via our website by clicking the button further below. If we collect your transactional information via Xero, or you provide us with the accounts information, you may not need to complete all the questionnaires. The questionnaires are designed as a prompt for you to let us know if something has changed during the year or if there will be some key information that we might need.

We would appreciate it if you could please take the time to read through the questions and worksheets that are relevant to your circumstances. Once you have gathered and collected all the required information, please email your completed questionnaires and supporting documentation through to the team at admin@aafl.nz. The sooner we have all of this information, the sooner we can complete your accounts and confirm your 2024 tax position and 2025 tax commitments. Questions? We can help

We’re happy to provide you with an update on how we are getting along, so feel free to ask at any time. We are generally working to a four week turnaround, so if you need your annual accounts sooner for likes of finance, please let us know. If you require any assistance, or have any queries about the questionnaires, please do give us a call on 04-970-1182. |

GOAL-SETTING FOR THE NEW FINANCIAL YEAR: PLANNING FOR SUCCESS |

|

|

The beginning of a new calendar year is an excellent time to review the year just finished, reflecting on what worked, what didn’t, and what changes you'd like to implement. By taking the time to plan, you can ensure that you are on track to achieving your financial goals and are well-prepared for any challenges that may arise.

To help make sure you can take advantage of the financial new year, we’ve gathered some goal-setting tips to consider below that are both simple and effective. |

| |

|

Your Yearly Business Review - Questions to consider - What were the most significant impacts on your business in the last 12 months? How well did you meet the challenges?

- What worked well last year? What systems, technology, products or services were successful?

- What accomplishments can you celebrate?

-

What situation, event or experience provided the biggest learning opportunity?

- What is the biggest challenge or frustration you face as you prepare for the year ahead?

- What did you most enjoy during the year? Do more of it. What did you least enjoy? Do less of it!

-

Analyse your financial reports. Are you earning what you'd like to? Is the business sustainably profitable?

Find your inspiration:

It’s always a good idea to start with the bigger picture and ask yourself what it is that you want to achieve through your business. What is it about the business that makes you jump out of bed every morning? Start broad and identify the driving force behind what you do. Is it to create wealth, or to are you planning on building up the business to resell at some point to make a profit? Whatever the reason, knowing the ‘why’ will help you gain clarity on your goals and allow you to start working towards them.

Pick something you can measure:

Vague goals aren’t as helpful as those you can measure and monitor (SMART Goals). Think about what you already measure in your business and how you’d like to see those metrics change. For example: - A 3% increase in net profit year-on-year

- A 2% reduction in expenses

-

1 new customer per month

- Reduce average payment time to under 50 days

- 4 weeks of holiday during which you don’t go into the office at all

Break it down:

Once you’re clear on your overarching goal or vision, then start breaking it down into smaller actionable steps. It’s a lot harder to achieve one large goal, and a lot easier making smaller incremental progress. For example, instead of setting yourself a lofty goal of tripling revenue over a number of years, plan out how that might eventuate by breaking it out into a series of smaller, actionable steps. For instance, the first of these steps might be to increase the range of products you sell if you run an ecommerce, or to increase revenue by 20% per quarter.

We can help:

While there are many metrics you could evaluate to track business performance, we’ve provided just a few ideas to inspire your business planning for a positive start to the year.

Whether you're a startup, a growing business, or an established enterprise, our team of knowledgeable accountants and business advisors is here to support and guide you every step of the way. We can help you review your goals and set a plan to accomplish them, propelling your business forward in 2024.

Ready to take your business to the next level? Let's make the next financial year your best one yet. If you’d like to chat about what you can do differently this year to enable your business to thrive, book a time with us today at 04 970 1182. |

|

|

INLAND REVENUE IMPORTANT NOTICES |

|

|

Inland Revenue Reviewing Covid Wage Subsidies

The Inland Revenue has now begun actively reviewing wage subsidies received by businesses throughout the COVID-19 period. This review involves reconciling these subsidies with the income tax returns that were filed.

In light of this review, we wish to alert you that if you received wage subsidies directly into your personal account, there is a possibility that these subsidies were not included in your income tax returns. This is because we were not aware of these specific transactions based on the information we have from you. Should you discover that subsidies were received but not accounted for in your tax returns, it is crucial that you contact us as soon as possible. By doing so, we can work with the Inland Revenue Department to rectify this, helping you avoid any potential penalty fees that may arise due to discrepancies in your tax return. If you require any assistance or further clarification regarding this matter, please call our team at 04 970 1182. |

NEW GST RULES AFFECTING SHORT-STAY ACCOMMODATION PROVIDERS |

|

|

Do you provide short-stay or visitor accommodation? As of April 1, 2024, new GST rules will now apply to you if you offer short-stay or visitor accommodations through third party providers such as Airbnb, Bookabach, and Holiday Houses. However, if you sell short-stay accommodations directly, for example, through your own website, these changes will not affect you.

If you are an accommodation host, it is important that you make sure you are aware of these new GST changes. |

| |

|

Here’s what you need to know:

The marketplace operator is responsible for collecting the GST, and how the new rules apply to you depends on whether you are GST registered or not. You must make sure your marketplace operator has your name, IRD number, and GST status. If you do not, they may treat you as non-GST-registered. Not GST-registered?

If you are not GST registered, the flat-rate credit scheme will apply. The marketplace operator will collect 15% GST on sales, 6.5% is returned to Inland Revenue, 8.5% is returned to you. GST-registered?

If you are GST registered, the marketplace operator will collect 15% GST on sales, and will return the GST to Inland Revenue on your behalf. (You must let the platforms you use know that you are GST registered). This will need to be accounted for in your GST returns as zero-rated supplies. To read more about this change, click the button below, which will redirect you to the Inland Revenue website.

If you have any questions or concerns, please contact the team at 04-970-1182 or send us an email at admin@aafl.nz. |

XERO: CLASSIC INVOICING IS RETIRING - 2 SEPTEMBER 2024 |

|

|

For some time now, Xero has offered its users two invoicing options: classic invoicing and new invoicing. However, in line with its ongoing commitment to innovation and to make way for enhanced features and improved functionalities, Xero has announced that it will retire the classic invoicing option, effective September 2, 2024. We understand that change can be an unsettling thing, but we assure you that Xero's new invoicing option is packed with time-saving tools designed to make invoicing more efficient. While some things may look a little different, all of your settings and invoice templates will seamlessly carry over. |

| |

|

If you are not already using new invoicing, now is the perfect time to make the switch. By familiarising yourself with the new version early on, you'll have plenty of time to adjust and get comfortable with the new interface. How do I make the switch:

You can make the switch to the new version of invoicing by clicking on the 'switch to new version', button in classic invoicing. You can also switch back to classic invoicing until it's retired, giving you the flexibility to choose which version works best for you. Xero also offers helpful resources and support to guide you through the transition process. What features can you expect in the new version?

Xero is continuously working on adding new features to the new version of invoicing. Before the retirement of classic invoicing, they will be incorporating many of the features that are currently available in classic invoicing, such as the ability to copy invoices to other documents, create overpayments, and view detailed history and notes. Additionally, there will be exclusive features in the new version, including more flexible invoice customisation tools, improved email templates for faster payments, and an easier way to personalise payment methods directly from your invoice.

We're here to help: If you need any assistance with the transition, please don't hesitate to contact our team on 04 970 1182. We're here to help. |

|

|

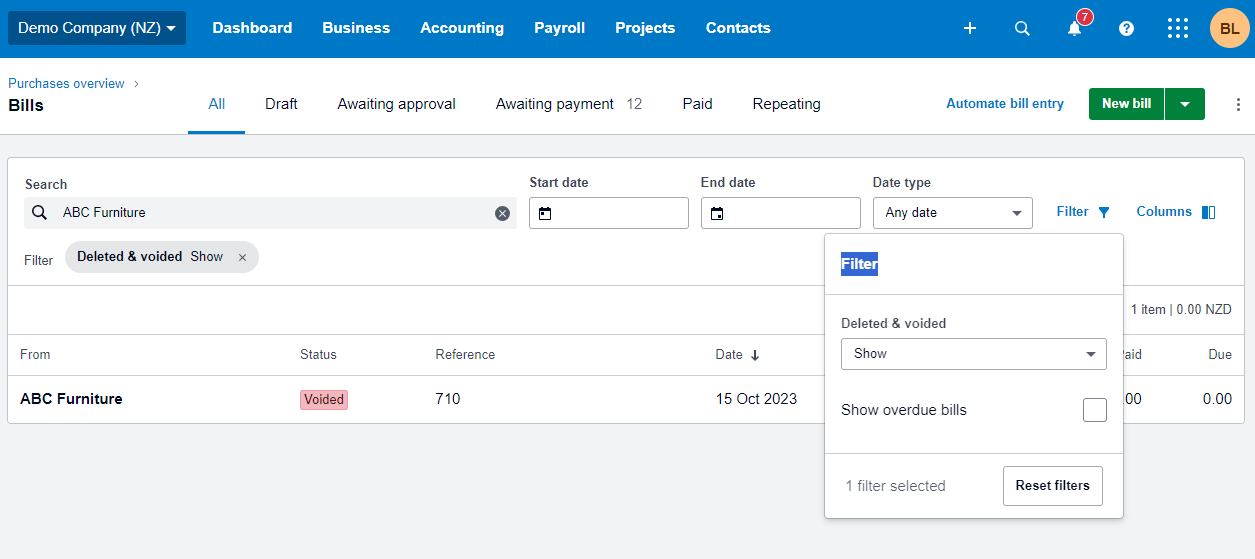

XERO TIP OF THE MONTH: RETRIEVE DELETED OR VOIDED BILLS |

Have you accidentally deleted a bill or voided a transaction and now need to retrieve the information? No problem! Just follow the simple steps below, and you'll be able to quickly locate your transaction within a matter of seconds. -

In the “Business” menu, select “Bills to pay”

- In the search bar, type the specific invoice details, which may include the company name, amount, or reference.

- Click on the "Filter" icon on the right-hand side next to "Columns."

-

Under the "Deleted & Voided" section, select "Show" from the drop-down menu and then click on the bill to open it.

- To retrieve the information, go to the right-hand side of the bill, click on "Bill Options," and then select "Copy."

- This can now be saved as a new bill

|

|

|

TAX QUESTION OF THE MONTH: |

QUESTION: A couple based in Christchurch purchased 2 inner city earthquake-damaged residential buildings in "as is" condition to use as long-term residential rental accommodation. They have spent significant money getting the buildings repaired and up to code. This has included significant engineering work. Is the work undertaken considered repairs or capital improvements?

If the work is generally considered capital improvements, what aspects could be separately identified and treated as repairs? ANSWER:

There are no specific provisions in the Canterbury Earthquake Recovery Act 2011 or the Income Tax Act 2007 that allow for deductions of capital expenditure incurred as a result of the Christchurch earthquakes. Therefore, you need to consider the usual “capital versus revenue” tests to determine the nature of the expenditure and whether or not this will be deductible.

The distinction between capital expenditure and revenue expenditure centres on the difference between the structure of a business (capital) and the regular conduct of the business (revenue). An expense that intends to produce an enduring benefit for the business is often regarded as being of a capital nature. Inland Revenue considers that the first stage of determining whether an amount is capital expenditure is identifying the relevant asset. The second stage is assessing the nature and extent of work done.

The asset itself is easily identifiable in this case, being the residential building. The work undertaken is described as involving significant expense and requiring significant engineering work. The costs are related to transforming the buildings to a state where they can be leased and earn income. This expenditure has provided an enduring benefit to the taxpayers. The nature and extent of the work completed is significant and has changed the nature of the building, as it was previously unfit for purpose. Therefore, the work carried out would be of a capital nature.

In addition, where a taxpayer acquires a property in a delipidated state (and presumably paying less for the property due to its delipidated state), incurring expenditure to restore the property to a useable state is considered to be capital in nature.

Inland Revenue generally considers expenditure is not deductible if it is incurred as part of a broad capital improvement project, –– even if, in isolation, the expenditure would be deductible repairs and maintenance. Therefore, for any expenditure to be deductible it would be necessary to show it was not part of the overall capital improvement project. |

|

|

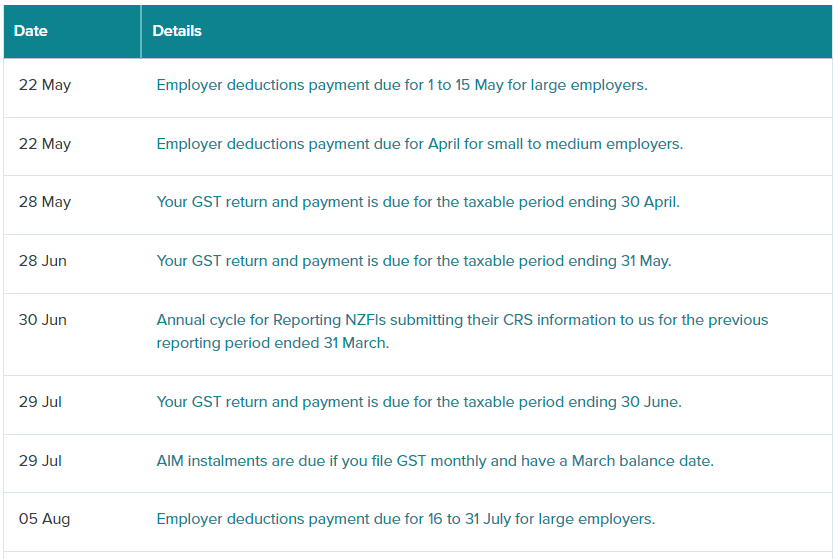

IRD UPCOMING TAX PAYMENT DATES |

|

|

|