Keep up-to-date with us and what's happening in the business world |

|

|

- Welcome 2023 - Review the Year That's Been and Plan for the Year Ahead - New GST Invoicing and Record-Keeping Requirements

- Using the Correct Prescribed Investor Rate - Xero Tip of the Month - Utilising the Xero App Store - Question of the Month: Income and GST deductions on holding costs when building is empty pending sale

- IRD Upcoming Tax Payment Dates |

|

|

We hope that everyone has had a wonderful holiday and is ready to embark on the new year ahead. The All Accounted For Team is back in full swing, ready to hit the ground running! We are all feeling energised, invigorated, and ready to assist with any business or tax queries you may have.

We would like to thank all of you, our valued clients, for your continued support throughout 2022. We understand that the past few years have been challenging for everyone, and we want you to know that we are here to support you and your business as we enter into a brand-new calendar year.

We look forward to working with you all again this year. |

| |

|

For business owners, this is often the time of year when you reflect on the progress made in the previous year to effectively plan for goals for the year ahead.

Last year, there were inescapable impacts on businesses, with some thriving, others failing, and others just getting by. So what kind of year was 2022 for your business?

Take the time to review the year and acknowledge all that has happened, good, bad or indifferent. Examining the year with an objective perspective can provide valuable insights to prepare for the next business year. Planning and goal setting will help provide a focus for your business efforts.

Your Yearly Business Review - What were the most significant impacts on your business in 2022? How well did you meet the challenges?

- What worked well last year? What systems, technology, products or services were successful?

-

What accomplishments can you celebrate?

- What situation, event or experience provided the biggest learning opportunity?

- What is the biggest challenge or frustration you face as you prepare for 2023?

- What did you most enjoy during the year? Do more of it. What did you least enjoy? Do less of it!

-

Analyse your financial reports. Are you earning what you’d like to? Is the business sustainably profitable?

Wondering how we can help your business plan for the upcoming year? While there are many metrics you could evaluate to track business performance, we’ve given you just a few ideas to inspire your business planning for 2023.

At All Accounted For we pride ourselves in offering our clients a progressive approach in all aspects of their business. Whether it's working through a financial model, providing support to execute your plans, or helping to identify your advantages - together, we can help you make headway to reach your business goals. When you conduct a past-year review with one of our experienced advisors, we will: - Run through your current business plan

-

Provide feedback on where you are heading and talk through the opportunities you might not see in your own business

- Provide valuable insights for this year's goal setting

- Implement a tailored business plan

Keen to learn more? We offer many business advisory services including: - Business Reporting: monthly, bi-monthly, or quarterly

- Cash Flow Forecasting

- Budgeting

- Business Valuations

-

Software Systems & Apps: setups and assistance

If you’d like to chat about what you can do differently this year to enable your business to thrive, give Ben Duflou or Sarah Toner a call on 04-970-1182 to discuss how we can help. |

NEW GST INVOICING AND RECORD-KEEPING REQUIREMENTS |

|

|

GST invoicing changes are coming! From 1 April 2023, new changes aimed at modernising GST rules for invoicing and record keeping are being introduced.

The new rules are designed to support e-invoicing and electronic record-keeping. There is no change to the GST calculation. These new rules may require you to update certain business processes and systems so please read on to learn how these changes may impact you. |

| |

|

Changes coming from 1 April 2023 include: - The requirement to use tax invoices is being replaced by a more general requirement to provide and keep certain records known as ‘taxable supply information’.

-

You'll no longer need to keep a single physical document holding the taxable supply information, such as a tax invoice, credit note, or debit note.

-

Your transaction records, accounting systems and contractual documents may, in combination, contain all the information you need to support the figures in your GST returns. However, as taxable supply information also includes tax invoices, you can keep using tax invoices if you wish.

-

The information you need to provide or keep depends on the value and the type of supply.

- Taxable supply information can be provided using an automated direct exchange between a buyer's and seller’s software, for example PEPPOL e-invoicing.

For more information and details around the new terminology, rules, and documentation requirements, please click the button below. |

|

|

USING THE CORRECT PRESCRIBED INVESTOR RATE |

Do you have a Portfolio Investment Entity (PIE)? Are you using the correct Prescribed Investor Rate (PIR) for your situation?

A prescribed investor rate (PIR) is the rate used to calculate how much tax you’ll pay on your portfolio investment entity (PIE) taxable income. Depending on your circumstances, you'll need to use a PIR that applies to your particular situation, so that you're paying the right amount of tax.

Having the correct PIR tax rate in place is essential to making sure your investments are taxed correctly so it is a good idea to review your PIR each tax year and let your portfolio investment entity (PIE) know of any changes to your income. Ideally, the IRD will detect any change based on your taxable earnings and then let you and your provider know. However, it is still your responsibility to ensure that you are using the correct rate.

What if my PIR code is incorrect? It is important that your PIR is set correctly because:

- If your PIR is too low, you'll be required to pay any shortfall as part of the income tax year-end process, and you may also be liable for penalties and interest. For example, if you advise your PIE fund manager that your PIR is 17.50% when actually is 28%, then less tax will be deducted than should be.

-

If your PIR is too high, you will end up paying more tax on your PIE investment income that you should, which while refundable by the Inland Revenue, will impact on your investment returns during the year.

What happens if I don't provide a PIR? If you do not notify your PIR to your fund manager, they will apply the default PIR of 28% to your PIE income. This rate could be higher than your PIR. We're here to help: For more information on using prescribed investor rates, click the below button to access the IRD PIR guidelines page or give us the AAF Team a call today on 04 970 1182. |

|

|

XERO TIP OF THE MONTH - UTILISING THE XERO APP STORE

|

Did you know that there are over 1000 apps that connect with Xero, providing fabulous options to extend the features available in Xero – all so you can profit from an integrated platform that promotes data flow over data entry?

Whether you're after a tool to help you with project management, inventory tracking, point-of-sale or management of bills and expenses, there is an app that can help you streamline the way you manage your business and increase efficiencies.

Discover apps at the Xero App Store by clicking the button below.

|

|

|

QUESTION:

A company has owned a single commercial rental property for over 20 years. About a year ago, its long-term tenant vacated the property. The directors initially sought a suitable new tenant to occupy the property, but eventually decided to simply sell it.

The property was put on the market and eventually sold after about 12 months. During this period that it was empty, the company incurred several expenses: rates, body corporate fees, power, and general maintenance totalling approximately $30,000.

Upon sale of the property, $150,000 of depreciation recovery income was included in the company’s tax return.

Can the company claim: - a deduction for the $30,000 of expenditure for income tax purposes?

- the GST on these expenses?

ANSWER: Income tax deduction

An income tax deduction for expenditure can be claimed when the general permission in s DA 1 of the Income Tax Act 2007 is satisfied and none of the general limitations in s DA 2 apply.

First, the income must be incurred in deriving assessable income or excluded income, or in carrying on a business to derive income of these natures. Expenditure incurred to derive rental income will satisfy the general permission.

However, as the commercial property in question was the sole property the company owned, the income stream ceased when the long-term tenant vacated the premises. The expenses incurred while the property was vacant and while the directors were not actively searching for a replacement tenant, would not be deductible.

This expenditure has not been incurred to derive income as the sale of the property gives rise to a capital gain. In addition, the expenditure was not incurred to derive depreciation recovery income, because this income arises from the reversal of previously claimed deprecation losses.

There is an argument that expenses incurred during the period that the directors were attempting to replace the tenant, and before deciding to sell the property, could be deductible. While there was no income stream at this point, the rental activity had not ceased, so the expenditure was incurred with the intention of deriving rental income in the future.

GST input tax claim

To claim input tax on the costs incurred, the good or service must be acquired for use in, or for the purpose of, making taxable supplies. The company was no longer supplying goods or services to another person for consideration when the tenant vacated. Arguably, it still has a taxable activity while a new tenant is sought as it retains the intention to make supplies of goods or services to another person for consideration.

Section 6(2) of the Goods and Services Tax Act 1985 provides that anything done in connection with the beginning or ending, including a premature ending, of a taxable activity is treated as being carried out in the course or furtherance of the taxable activity. Accordingly, expenditure incurred while the company is seeking to sell the building (assuming the sale is a taxable supply) can be considered incurred in carrying on its taxable activity. Therefore, GST should be claimable on this expenditure when incurred.

So if you have a building or property that is currently vacant and you are not actively attempting to rent it, there may be a question mark around the deductibility of the expenses. If this situation applies to you, please contact us today to discuss in more details to ensure the right taxation treatment is applied. |

|

|

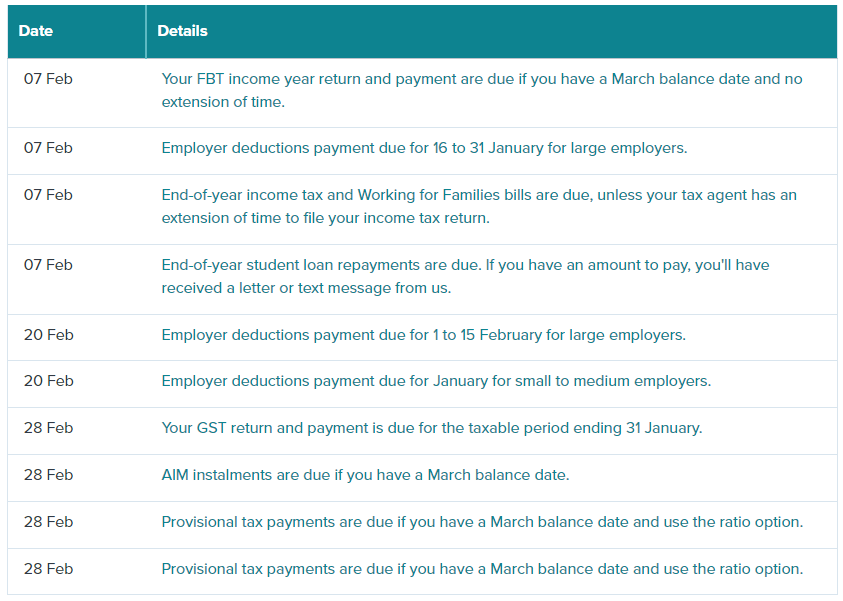

IRD UPCOMING TAX PAYMENT DATES |

|

|

|